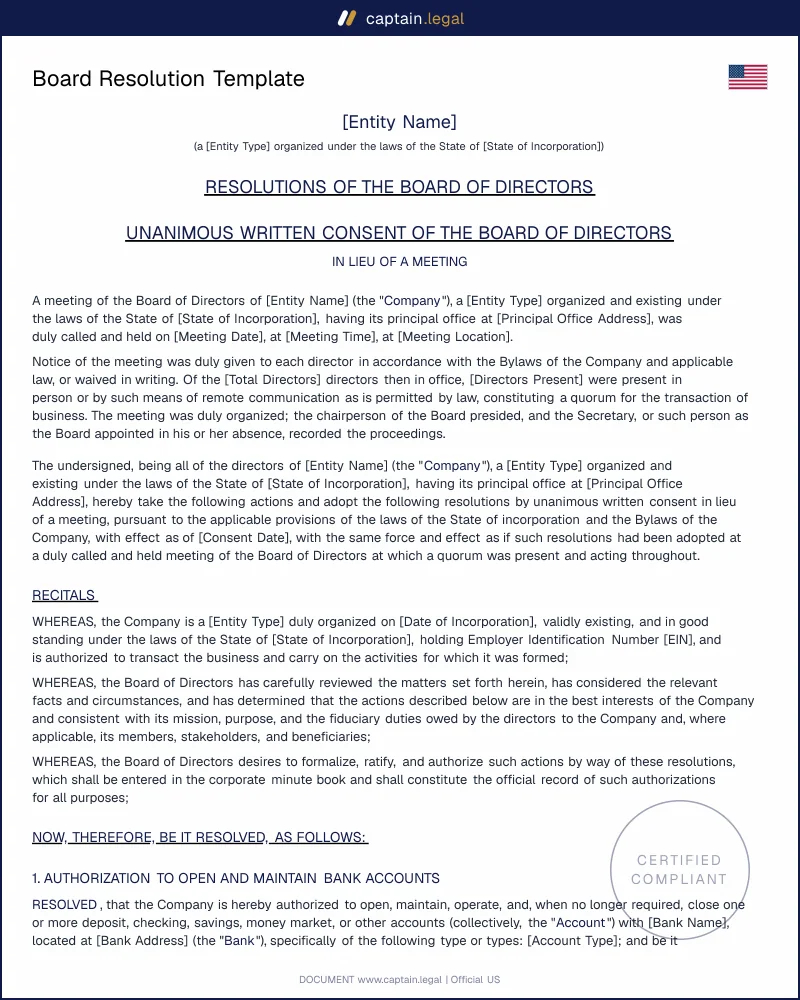

A board resolution is the written record a US nonprofit or corporation uses to formalize a decision made by its board of directors. It is the one-page (or two-page) document a bank asks for before opening an account in the entity's name, the proof a grantmaker wants before wiring restricted funds, and the trail an IRS examiner follows when reviewing executive compensation or related-party transactions. Whether the decision concerns opening a checking account, hiring an executive director, approving an annual budget, or authorizing a real estate purchase, the resolution is what turns an informal vote around a conference table into a legally binding act of the organization. This template is built for US nonprofits and small corporations that need a clean, lawyer-grade corporate resolution without paying a firm to draft it from scratch.

Compliant

2026 Legislation

50,000+ clients

trust us

Affordable

From $4.90 / doc

Secure payment

Instant download

US Board Resolution Template | Bank Account, Hiring, Budget

Secure payment

What is a board resolution?

A board resolution is a formal written statement adopted by the board of directors of a corporation or nonprofit, recording a specific decision and authorizing one or more officers to act on it. In practice it sits between two other documents people often confuse it with. Meeting minutes describe the entire discussion at a board meeting, including motions, debate, attendance, and votes. A written consent is the mechanism used when directors approve something without holding a formal meeting, typically requiring unanimous signatures under most state statutes. A board resolution, by contrast, captures the operative language of a single decision and is usually extracted from minutes or signed as a standalone written consent.

The format is conservative on purpose. Banks, title companies, the IRS, and state regulators are looking for three things : a clear statement that a properly constituted board met or signed off, the exact text of what was approved (the "RESOLVED that…" clause), and the identification of which officer is authorized to execute documents on the organization's behalf. Most US nonprofits incorporated under state law operate under a Model Nonprofit Corporation Act framework, and that statutory template assumes the board acts through resolutions whenever it exercises its corporate powers. A decision that is not memorialized this way can still be valid internally, but it becomes very hard to enforce against third parties who never saw a piece of paper. If a third party is going to rely on the decision, the resolution is what they will ask to see.

Legal framework

US board resolutions live at the intersection of three legal regimes. The first is your state nonprofit corporation statute, which governs how the board is constituted, how it votes, and what kinds of decisions require board action rather than officer discretion. Most states have adopted some version of the Model Nonprofit Corporation Act, with significant local variations in California (Corporations Code §§ 5210–5238), New York (Not-for-Profit Corporation Law §§ 701–717), Delaware (Title 8, Chapter 1 for stock corporations; Title 5 for nonstock), and Texas (Business Organizations Code Chapter 22). These statutes set the quorum requirements, the rules for meetings by telephone or video, and the conditions under which directors can act by unanimous written consent in lieu of a meeting.

The second layer is federal tax law. For organizations recognized under Internal Revenue Code § 501(c)(3), the IRS does not directly require resolutions, but it does require that key decisions be properly authorized and documented. The IRS's published guidance in Governance and Related Topics for 501(c)(3) Organizations explicitly ties good board documentation to compliance with the prohibitions on private inurement and improper private benefit. Executive compensation, transactions with insiders, and grants to related entities are precisely the decisions where a contemporaneous, well-drafted resolution is the difference between a clean Form 990 and an intermediate sanctions problem under § 4958.

The third layer is the organization's own articles of incorporation and bylaws. The bylaws typically specify which decisions require a simple majority, which require a supermajority, and which categories of officers can sign on behalf of the entity. A resolution that contradicts the bylaws is voidable, even if every director signed it. Before adopting any resolution that touches signing authority, financial limits, or amendment of governing documents, the secretary should pull the corporate bylaws template language for the specific decision type and confirm that the threshold is being met.

When do you need this document?

The most common trigger is the opening of a bank account in the entity's name. Every US bank, without exception, requires a signed board resolution naming the authorized signers, the type of account, and any spending or transfer limits before it will open business or nonprofit accounts. Banks have been burned too many times by unauthorized signers draining accounts, so they treat the resolution as their primary defense. A second trigger, equally frequent, is the hiring or compensation of a senior officer, particularly the executive director, CEO, or CFO. For 501(c)(3) organizations, Treasury Regulation § 53.4958-6 establishes a rebuttable presumption of reasonableness for executive compensation, but only if the board approves the pay in advance, relies on comparability data, and records the basis for its decision in a contemporaneous resolution. Skipping the resolution does not just look sloppy ; it costs you the safe harbor.

Annual budget approval is a recurring use. Most nonprofits adopt their operating budget by board resolution at the start of each fiscal year, which both satisfies the bylaws and creates the audit trail funders increasingly demand. The same applies to budget amendments mid-year. Beyond money, resolutions are used to authorize the signing of leases and major contracts, the appointment of officers and committee members, the acceptance of restricted gifts, and the formal adoption of policies like conflict-of-interest, whistleblower, and document retention rules.

One edge case worth flagging : if you are forming a new nonprofit, the very first set of decisions, taken at the organizational meeting before any operations begin, should be captured as resolutions. That initial package typically accompanies your articles of incorporation filing and is referenced years later when the IRS, banks, or auditors ask how the organization got started.

Key clauses included in our template

- The recital block identifies the corporation, the date of the meeting or written consent, the directors present or signing, and confirms that a quorum was established under the bylaws. This is the section banks and auditors read first ; if the quorum is not stated, the resolution is treated as suspect even when the substance is fine.

- The operative resolution clause, traditionally introduced by "RESOLVED, that…", contains the actual decision in a single, declarative sentence. Our template uses the conservative "RESOLVED, FURTHER…" chain when multiple related decisions are bundled, so each authorization can be cited independently later without rewriting the document.

- The authorization to act clause names the officer or officers empowered to sign contracts, open accounts, file documents with state or federal agencies, and take any further steps consistent with the resolution. This clause is what a bank or counterparty actually relies on, so it has to identify the officer by title and, where useful, by name.

- The certification by the secretary at the bottom of the document is what gives the resolution evidentiary weight outside the organization. The secretary (or assistant secretary) attests that the resolution was duly adopted, is currently in effect, and has not been amended or rescinded. Without this certification, third parties may demand the full minutes.

- A conflict-of-interest acknowledgment, included as an optional block, records that any director with a financial interest in the matter disclosed the interest, abstained from the vote, and that the remaining disinterested directors approved the action. This is the language the IRS expects to see whenever a 501(c)(3) approves a transaction with an insider.

- The effective date and counterpart signature provisions handle the practical reality that written consents are often signed in different cities or time zones, and that some resolutions are intended to take effect prospectively (a budget adopted in December for the following fiscal year, for example).

State-specific considerations

California nonprofits operate under the Nonprofit Corporation Law (Corporations Code, beginning at § 5110 for public benefit corporations). Section 5211 sets a default quorum of a majority of authorized directors, which the bylaws can lower but only to one-fifth or five directors, whichever is larger. California is also unusual in that Corporations Code § 5233 imposes specific procedures for self-dealing transactions, requiring not just disclosure and abstention but also a board finding that the transaction is fair to the corporation. A California resolution approving a contract with a related party that omits the fairness finding is exposed to later challenge by the Attorney General, who actively polices nonprofit governance through the California employment and corporate templates ecosystem of compliance documentation.

Texas nonprofits fall under Business Organizations Code Chapter 22. Section 22.220 allows written consents in lieu of a meeting if signed by the number of directors that would constitute a quorum at a meeting, which is more permissive than the unanimous-consent default in many states. Texas also enforces § 22.230 on indemnification, and any resolution authorizing an officer's indemnification or advancement of expenses must track the statutory language precisely. The Secretary of State does not file resolutions, but banks and the Texas Comptroller will ask for them whenever sales tax exemption, unemployment tax registration, or franchise-tax filings are at stake.

Florida applies Chapter 617 of the Florida Statutes to nonprofit corporations. The quorum default under § 617.0824 is a majority of directors in office, and Florida explicitly authorizes board action by "any means of communication by which all directors participating may simultaneously hear each other," which is broader than some states' video-only language. Florida charities soliciting contributions must also register with the Department of Agriculture and Consumer Services under § 496.405, and the registration form asks for board-adopted policies that should themselves be supported by resolutions.

New York is the most procedurally demanding of the major states. The Not-for-Profit Corporation Law requires that the chair of a meeting and the secretary taking minutes be different people (§ 712-a), and the Charities Bureau of the Attorney General routinely reviews resolutions during merger, dissolution, and asset-sale approvals under § 510 and § 511. Resolutions touching real property transactions or substantial asset transfers in New York should be drafted with the expectation that the Charities Bureau will read them word for word.

How to fill out this board resolution

The template is built around a guided flow that starts with the organizational identity : entity name as it appears on the articles of incorporation, state of formation, principal office, and tax classification (501(c)(3), 501(c)(4), 501(c)(6), or for-profit corporation). From there, the form adjusts the statutory citations and recital language to match the governing state law, so a California resolution will reference Corporations Code § 5211 automatically and a Texas resolution will pull § 22.220. You then select the decision type from a menu : bank account, executive compensation, budget approval, contract authorization, officer appointment, real estate, policy adoption, or custom language.

The next step is the meeting or consent block. You indicate whether the resolution was adopted at a meeting (in which case the template prompts for date, location, directors present, and vote count) or by written consent (in which case it prompts for the signature page and effective date). For 501(c)(3) organizations, an optional conflict-of-interest sub-flow appears whenever the decision type involves compensation, related-party transactions, or asset transfers ; completing it adds the Treasury Regulation § 53.4958-6 safe-harbor language to the document. The final step is the secretary's certification, which the template formats correctly with a signature block and an optional corporate seal placeholder for personal documents styling preferences. The output is delivered in both Word (for ongoing editing) and PDF (for execution and archiving) without further conversion steps.

Common mistakes to avoid

The single most common mistake is treating the resolution as a formality and copying boilerplate from a generic template without adjusting the recitals. A resolution that says "WHEREAS, a quorum was present" without naming the directors who attended or signed is unenforceable on its face. Banks will reject it, auditors will flag it, and a litigant challenging the underlying action will use the gap as their opening argument. The second mistake, particularly damaging for 501(c)(3) organizations, is approving executive compensation or insider transactions without the conflict-of-interest procedure recorded in the resolution itself. The rebuttable presumption of reasonableness under § 53.4958-6 is procedural ; if the documentation does not exist on the day of the vote, the safe harbor is gone and reconstructing it later is treated by the IRS as suspect.

A third recurring mistake is granting open-ended authority to an officer without numerical limits. "The Treasurer is authorized to enter into contracts on behalf of the corporation" is vastly different from "The Treasurer is authorized to enter into contracts not exceeding $50,000 in aggregate annual commitment." The first creates unlimited exposure ; the second creates a controlled delegation. Closely related is the failure to align the resolution with the bylaws. If the bylaws require a two-thirds vote to approve real estate transactions and the resolution shows a simple majority, the action is voidable regardless of how clearly the resolution is drafted. The last frequent error is forgetting to revoke or amend prior resolutions when the same subject is revisited. A bank that holds an old resolution naming a departed treasurer as a signer will continue to honor that signer's authority until a new, certified resolution arrives. Letting the paper trail drift is how unauthorized payments happen.

Frequently Asked Questions

31 verified reviews · 50 000+ downloads

- Immediate access to the document

- PDF + Word download

- Compliant with 2026 legislation

- Reviewed by lawyers

You might also like