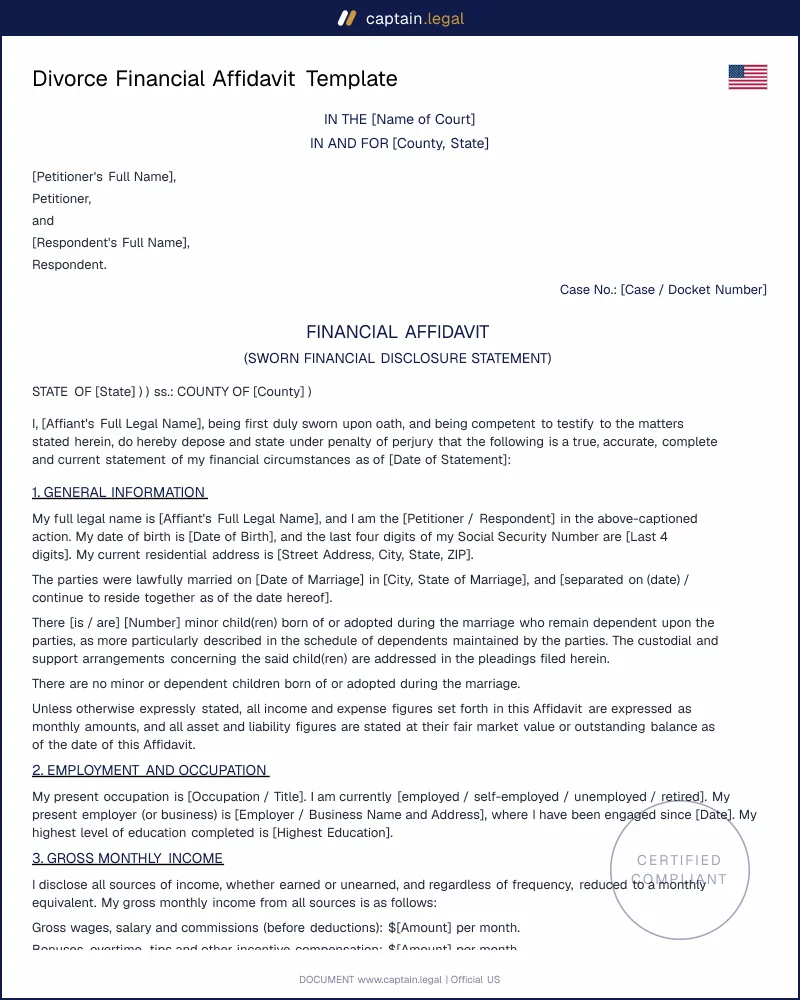

California uses the Income and Expense Declaration, Form FL-150, together with the Declaration of Disclosure under Family Code §§2104 and 2105. The state requires both a preliminary and a final declaration, and you must serve, not file, your tax returns for the prior two years alongside the form. California courts impose significant monetary sanctions for incomplete disclosure, and the duty to disclose continues throughout the case as your circumstances change. A spouse protecting business assets often coordinates this filing with broader business formation and ownership documents that establish entity value.

Florida mandates the Family Law Financial Affidavit, Form 12.902(b) for the short form under the income threshold and Form 12.902(c) for the long form above it, filed within 45 days of the petition. Under Rule 12.285, the affidavit itself cannot be waived even when both parties agree to skip other disclosures. The form must travel with three years of tax returns, pay stubs, and account statements, and objections to disclosure must be filed at least five days before the due date.

New York requires the Statement of Net Worth under DRL 236(B)(4), a sworn document covering income, expenses, assets, and liabilities that must be signed before a notary despite the 2023 amendment to CPLR 2106. New York applies equitable distribution, so the form's careful separation of marital from separate property carries real weight in how assets divide. The statement must generally be filed within 20 days of a request.

Texas does not use a single statewide affidavit form. Instead, parties typically file a sworn Inventory and Appraisement listing community and separate property and debts, and many counties impose their own local disclosure rules under the Texas Rules of Civil Procedure. Because Texas is a community property state, accurate characterization of each asset as community or separate is the central drafting task.