A purchase agreement is the binding contract that turns a verbal handshake on a property into an enforceable transfer of title. It records the price, the conditions the buyer and seller agree to honor before closing, and the remedies available if either side walks away. In residential transactions across the United States, this single document does more legal work than any other paper signed during the deal, and it is the instrument every title company, lender, and closing attorney will read line by line.

Most buyers and sellers reach for a real estate purchase contract once an offer has been verbally accepted. The form's job is to lock the deal down before a competing bidder appears, and to give both sides a written roadmap from the accepted offer to the recorded deed. The template at Captain.Legal covers single-family homes, condominiums, townhouses, and vacant residential lots, with state-specific language built into every clause that requires it.

Compliant

2026 Legislation

50,000+ clients

trust us

Affordable

From $4.90 / doc

Secure payment

Instant download

Purchase Agreement Template | PDF & Word | All 50 States

Secure payment

What is a purchase agreement?

A purchase agreement is a written contract by which a seller commits to transfer ownership of real property to a buyer in exchange for a stated price, on terms that both parties accept before closing. It is sometimes called a real estate purchase contract, a residential purchase and sale agreement, or simply a PSA. Whatever the local label, the document performs the same function: it converts a non-binding offer into a binding obligation, opens the inspection and financing windows, and triggers the escrow timeline that ends with a recorded deed.

The contract is not the deed. Signing a purchase agreement does not transfer title. Title passes only when the closing occurs and the deed is recorded with the county recorder's office. Between signature and closing, the buyer holds equitable title and the seller holds legal title, a distinction that matters if the property burns down, is damaged, or is hit by a lien before the keys change hands. The risk-of-loss clause, addressed below in the Key clauses section, is the contractual answer to that vulnerability.

A common confusion is the difference between a purchase agreement and a letter of intent. A letter of intent expresses interest and outlines the deal's economic shape ; it is generally non-binding except for confidentiality and exclusivity provisions. The purchase agreement is the real contract, fully enforceable, with damages available if a party defaults. Buyers using a residential lease agreement template for a rent-to-own arrangement should know that a separate purchase agreement is still required to consummate the sale at the end of the lease term.

Legal framework

Real estate sales in the United States are governed primarily at the state level, with federal law layered on top for fair housing, lending disclosures, and environmental hazards. The cornerstone is the Statute of Frauds, in force in every state, which requires any contract for the sale of an interest in real property to be in writing and signed by the party against whom enforcement is sought. An oral agreement to sell a home is unenforceable in court no matter how many witnesses heard it, and that rule alone explains why no closing attorney will accept a deal without a signed contract in the file.

State-level statutes set the disclosure obligations that the seller must satisfy. California's Transfer Disclosure Statement under Civil Code §1102 is the most demanding ; Texas requires the Seller's Disclosure Notice under Property Code §5.008 ; Florida applies the common-law duty articulated in Johnson v. Davis (Fla. 1985), which obliges sellers to disclose known material defects ; New York imposes the Property Condition Disclosure Statement under Real Property Law §462. The Cornell Legal Information Institute's overview of real estate sales contracts under U.S. property law gives a useful federalism-level view of how these state regimes interlock.

Federal law adds two layers that show up on every residential contract. The Residential Lead-Based Paint Hazard Reduction Act (commonly called Title X) requires sellers of homes built before 1978 to deliver an EPA lead-paint disclosure and to allow a 10-day inspection window. The Real Estate Settlement Procedures Act (RESPA) and the TILA-RESPA Integrated Disclosure rule shape how the lender's Loan Estimate and Closing Disclosure dovetail with the contract's contingency dates. Miss the three-business-day TRID delivery window and the closing date moves automatically, with consequences for any rate lock or moving truck already booked.

When do you need this document?

The most frequent trigger is an accepted offer on a primary residence. A buyer's agent emails the listing agent, the seller signs off on price and terms, and within hours the parties need a written contract to lock the deal before a competing bidder shows up. The purchase agreement turns the verbal acceptance into an enforceable obligation and starts the clock on inspection, financing, appraisal, and title contingencies. Without the signed document, the seller can entertain backup offers without consequence and the buyer has no claim on the property.

For sale-by-owner (FSBO) transactions are the second classic scenario. When no real estate broker is involved, the parties have no agent-supplied form to fall back on, and the risk of an enforceable but defective contract is real. A direct link between neighbors, family members selling to children, or investors buying off-market all sit in this category. The same template is used whether the price is paid in cash, financed by a conventional mortgage, or carried by the seller through a purchase money mortgage recorded at closing.

Investor flips and rehab purchases are the third common use. An investor under contract on a distressed property needs an assignment clause baked into the agreement so the contract can be assigned to a new buyer before closing. Wholesalers depend on this mechanism every day, and a contract drafted without it leaves the wholesaler unable to monetize the deal. Check your state's wholesaler licensing rules first : Illinois, Oklahoma, and Pennsylvania have all tightened wholesale activity in recent years, and the contract is not a licensing shield.

A fourth situation worth flagging is the rent-to-own conversion at the end of a lease. Tenants who started with a month-to-month rental agreement and exercise an option to purchase need a separate purchase agreement to actually transfer title ; the lease option alone does not move the deed. One last edge case : land sales where the buyer plans to build. The contract should include a due diligence period long enough to confirm zoning, utilities, and septic feasibility before the earnest money goes hard.

Key clauses included in our template

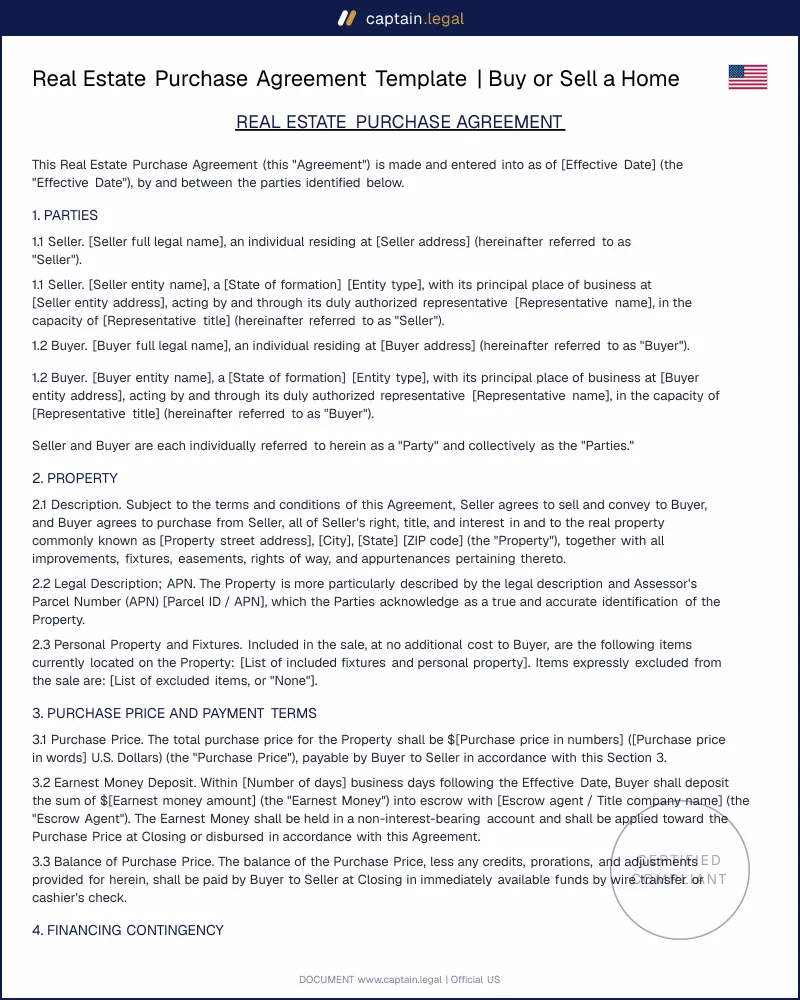

- The identification of the parties and the property opens the contract with full legal names of every buyer and seller, the property's legal description (lot, block, subdivision, or metes-and-bounds, depending on state custom), the Assessor's Parcel Number, and the street address. A description that relies only on the postal address has been struck down in courts as too vague to satisfy the Statute of Frauds. Sellers transferring through a quitclaim must use the formal description from their existing quitclaim deed template to keep the chain of title clean.

- The purchase price and earnest money deposit state the agreed price, the deposit amount (commonly between one and three percent of the price), the escrow agent holding it, and the conditions under which it becomes non-refundable. The clause distinguishes between liquidated damages on default and the broader remedy of specific performance, which several states limit by statute.

- The financing contingency allows the buyer to terminate without losing the deposit if a mortgage is not approved within a set window, typically 21 to 30 days. The clause specifies the loan type (conventional, FHA, VA, USDA), the maximum interest rate the buyer is willing to accept, and the deadline for loan commitment. A buyer who lets the contingency lapse without notice is treated as having waived it.

- The inspection and due diligence contingency opens a window, generally 7 to 17 days, during which the buyer can hire inspectors, request repairs, negotiate credits, or terminate the contract. The state-specific as-is riders (popular in Florida and Arizona) limit the seller's repair obligations while preserving the buyer's right to walk.

- The title and survey clause requires the seller to deliver marketable title free of liens other than those expressly accepted, sets a deadline for the buyer's title objection, and identifies the title company that will issue the owner's policy. Defects revealed by the title commitment trigger the seller's cure period.

- The closing, possession, and risk of loss provisions fix the closing date, allocate transfer taxes and recording fees according to local custom, and decide who carries the casualty risk between contract and closing. Most state forms place the risk on the seller until possession is delivered.

State-specific considerations

California. The state operates almost exclusively on the California Residential Purchase Agreement and Joint Escrow Instructions (the CAR RPA), but a custom contract is fully enforceable as long as it satisfies Civil Code §1102 disclosure duties and the Natural Hazard Disclosure Statement under §1103. Earthquake fault zones, fire severity zones, and flood hazard areas all trigger statutory disclosures that the contract should attach as exhibits. California also enforces the Mello-Roos Community Facilities Act disclosure for any property within a special tax district, and a missing Mello-Roos statement gives the buyer a three-day rescission right after delivery.

Texas. The Texas Real Estate Commission (TREC) publishes promulgated forms that licensed agents must use, but FSBO sellers and attorneys are not bound to them. Whichever form is used, Property Code §5.008 requires the Seller's Disclosure Notice before contract execution, and the Texas Residential Construction Liability Act shapes the post-closing remedy for defects in homes less than ten years old. Texas is a community-property state, and a married seller's spouse must join the contract and the deed even when the spouse's name is not on title, a trap that recurs in FSBO closings.

Florida. Florida courts read the contract strictly under Johnson v. Davis, which makes any known and material defect that is not readily observable a disclosure obligation regardless of as-is language. The Florida Building Code sinkhole disclosure under §627.7073 applies to any property where a sinkhole claim has ever been paid, and the Construction Defect Notice Law in Chapter 558 governs new-construction claims. Properties in coastal counties trigger the Coastal Construction Control Line disclosure, with separate requirements for windstorm and flood insurance binders before closing.

New York. New York is unusual in routing most residential closings through attorneys rather than title companies, and the contract is typically negotiated by counsel after the initial binder or offer letter. The Property Condition Disclosure Statement under Real Property Law §462 gives the buyer a $500 credit at closing if the seller refuses to deliver it, an oddity that pushes most sellers to opt out by paying the credit rather than warranting condition. New York City co-op transactions add a board approval contingency layered on top of the standard contingencies, which the contract must accommodate.

How to fill out this purchase agreement

You start by selecting the state where the property is located. From there, the form adjusts disclosure exhibits, statutory citations, and the default contingency periods to match local practice : California pulls the Mello-Roos and Natural Hazard riders, Texas pulls the Seller's Disclosure Notice under §5.008, Florida adds the as-is rider and sinkhole disclosure where relevant. The next section asks for the legal description of the property, the Assessor's Parcel Number, and the names of every buyer and seller exactly as they appear on the existing deed.

Price and money terms come next. You enter the purchase price, the earnest money amount, the escrow holder, the financing structure (cash, conventional, FHA, VA, or seller-carry), and the contingency windows for financing, inspection, appraisal, and title. The form proposes industry-standard durations and lets you tighten or extend each one. Possession date, prorations of taxes and HOA dues, and the allocation of transfer taxes are entered against state-default conventions you can override.

The final pass handles personal property included in the sale (appliances, fixtures, window treatments), riders for lead-paint, radon, septic, and well water where applicable, and the signature blocks for buyers, sellers, and any required spousal joinder. Once you review the generated PDF, you download both Word and PDF versions, sign electronically or in wet ink, and deliver counterparts to the escrow agent. Your account on Captain.Legal keeps the executed contract available for download throughout the transaction, which matters when the lender or title company asks for a clean copy three weeks into escrow.

Common mistakes to avoid

The first and most expensive mistake is leaving the legal description blank or relying on the street address. Title companies will not insure a deed whose underlying contract describes the property only as "123 Main Street" when the parcel actually spans two recorded lots, and the closing collapses while everyone scrambles to amend. Pulling the description from the seller's prior deed, or from the quitclaim deed template used in the chain of title, is the simple fix that almost no FSBO seller remembers to do. A close cousin of this error is mismatched names : the deed on record reads "Robert J. Smith and Mary Smith, husband and wife" but the contract names "Bob Smith" alone, and the title company refuses to close without an affidavit of identity.

Earnest money handling is the second recurring trap. Sellers occasionally insist on receiving the deposit directly rather than through an escrow agent, which exposes the buyer to total loss if the deal cracks and the seller refuses to refund. The third mistake is letting contingency dates pass without written notice. Most state forms treat silence as waiver, and a buyer who finds black mold on day 11 of a 10-day inspection contingency has lost the right to terminate. Fourth, the time is of the essence clause is often left in by default without anyone reading it ; once it is in the contract, missing the closing date by a single day is a material breach. Last, sellers in community-property states routinely forget to bring the non-titled spouse to signing, and the contract becomes unenforceable until the spouse joins the agreement or executes a quitclaim.

Frequently Asked Questions

71 verified reviews · 50 000+ downloads

- Immediate access to the document

- PDF + Word download

- Compliant with 2026 legislation

- Reviewed by lawyers

You might also like