A promissory note is a written, signed promise by one person (the maker) to pay a fixed sum of money to another (the payee), either on demand or on a specific date. In its purest form, it is the oldest contract in commerce. You borrow, you sign, you pay. The reason private lenders, family members, and small business owners still rely on it in 2026 is simple: when drafted correctly under UCC Article 3, the note becomes a negotiable instrument, enforceable in any U.S. court with minimal proof beyond the signed paper itself.

This page covers the standard promissory note between individuals (sometimes called an IOU agreement or personal loan agreement), with a payment schedule, the statutory interest rate of the lender's state, default and acceleration clauses, and a cosigner block. The template is drafted for all 50 states, with state-specific usury caps and notarization rules built into the form.

Compliant

2026 Legislation

50,000+ clients

trust us

Affordable

From $4.90 / doc

Secure payment

Instant download

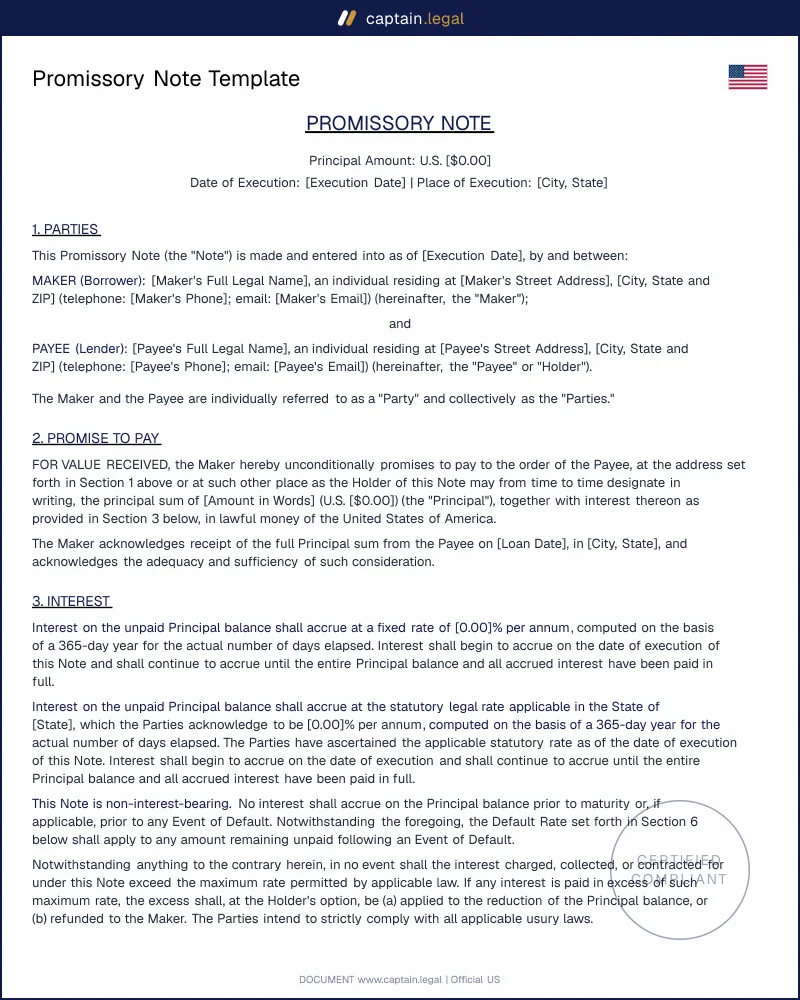

Promissory Note Template — Personal Loan Agreement with Cosigner

Secure payment

What is a promissory note?

A promissory note is a unilateral instrument. Only the borrower signs it ; the lender's countersignature is optional and adds nothing to enforceability. That single-signature structure is what distinguishes a note from a loan agreement, which is a bilateral contract negotiated and signed by both parties. In practice, most personal loans use a note because the terms are simple enough to fit on two pages, and because §3-104 UCC gives a properly drafted note the status of a negotiable instrument, meaning the holder can sue on the paper alone without producing the underlying transaction.

The note differs from an IOU in a way that matters in court. An IOU acknowledges a debt but does not promise to repay it on stated terms ; judges treat it as evidence, not as the contract itself. A promissory note contains the four elements §3-104 requires : an unconditional promise to pay, a fixed sum, payable on demand or at a definite time, and payable to order or to bearer. Drop any of these elements and you still have a valid personal loan agreement, but you lose negotiable-instrument status, the holder in due course doctrine, and the simplified collection procedures that come with them.

The note also differs from a secured promissory note, which couples the promise to pay with a security interest in collateral (a vehicle title, equipment, a deed of trust on real property). The template on this page is the unsecured version. If your loan exceeds $10,000 or involves a vehicle, switch to the secured variant or pair the note with a separate security agreement.

Legal framework

Promissory notes between individuals are governed by a layered framework. At the foundation sits Article 3 of the Uniform Commercial Code, adopted with minor variations by every state and the District of Columbia. §3-104 UCC defines what makes a note negotiable. §3-118 UCC sets the federal-baseline statute of limitations for actions on notes : six years from the due date of the last installment, or from acceleration, whichever applies. §3-309 UCC tells you what to do if the note is lost or destroyed before payment, which happens more often than people think. For the official text and official comments, see the Cornell Legal Information Institute's edition of UCC Article 3, the standard reference cited by federal and state courts.

Layered over the UCC are state usury statutes, which cap the interest rate a private lender can charge a non-corporate borrower. The numbers vary widely and are revisited every legislative session. California Civil Code §1916-1 caps non-exempt personal loans at 10 % per year on the unpaid balance. Texas Finance Code §302.001 sets the default rate at 6 % when the parties have not agreed in writing and authorizes up to 10 % when they have, with higher tiers for licensed lenders. New York General Obligations Law §5-501 caps civil usury at 16 % and treats anything above 25 % as criminal usury under Penal Law §190.40. Florida's §687.03 Fla. Stat. allows up to 18 % on loans under $500,000, with criminal usury kicking in above 45 % per year. Charging an interest rate above the state cap can void the entire interest obligation and, in several states, the principal as well. Drafting the note without checking the lender's home-state ceiling is the single most common error among private lenders.

A third layer applies when the note is paired with collateral : Article 9 UCC governs the creation and perfection of the security interest, and a UCC-1 financing statement must be filed with the relevant Secretary of State to make the security interest enforceable against third parties. For real-estate-backed notes, you are now in mortgage or deed of trust territory, with recording requirements that vary by county. The template on this page is unsecured and stops short of that complexity.

When do you need this document?

The most common use is a family or friend-to-friend loan, typically between $500 and $50,000. A parent advances a down payment to a child buying a first home, a sibling fronts startup capital, a friend covers an unexpected medical bill with the expectation of being paid back. People resist signing a note in these situations because it feels cold, but the absence of a written instrument is precisely what poisons relationships when repayment slows. A signed note converts a vague expectation into a documented schedule, and it gives the IRS a paper trail that prevents the loan from being reclassified as a taxable gift under the imputed-interest rules of §7872 IRC.

The second frequent scenario is seller financing on a private vehicle, boat, or equipment sale. The buyer cannot or does not want to use bank financing, and the seller accepts installment payments. Here the note is almost always paired with a vehicle bill of sale and, ideally, a security agreement on the title. Without the security interest, the seller is just an unsecured creditor in line behind every other claim on the buyer's assets.

A third use is the founder loan to a small business, where an owner injects personal funds into an LLC or corporation. Booking the advance as a loan rather than a capital contribution preserves the owner's right to be repaid before distributions and produces a deductible interest expense for the entity. The note should match the corporate authorization in the LLC operating agreement or board minutes, otherwise the IRS may recharacterize the advance as equity.

Two edge cases deserve attention. Demand notes (payable "on demand" rather than on a schedule) trigger the statute of limitations from the date of issuance in some states, meaning a six-year-old demand note may already be unenforceable even though the lender has never asked for payment. And notes signed by a married borrower in a community-property state (CA, TX, AZ, ID, LA, NM, NV, WA, WI) may bind the marital estate unless the non-borrowing spouse explicitly disclaims by separate writing.

Key clauses included in our template

The template is drafted to satisfy §3-104 UCC on every clause that matters for negotiability, while remaining readable to non-lawyers.

- The identification of the parties names the maker (borrower) and the payee (lender) with full legal names as they appear on government-issued ID, current addresses, and, when relevant, the entity capacity in which they sign. A note signed by "John Smith, Manager" without identifying the LLC has been treated as personal liability in dozens of cases.

- The principal amount and disbursement clause states the loan amount in figures and in words (the words control if the two disagree, under §3-114 UCC) and records the date and method of disbursement (wire, check, cash). The disbursement record is what prevents the borrower from later claiming the funds were a gift.

- The interest rate and computation method specify the annual rate, whether it is simple or compound, the day-count convention (actual/365, 30/360), and a fallback to the lender's state statutory rate if the contractual rate is found unenforceable. A built-in usury savings clause caps the effective rate at the state maximum.

- The payment schedule is drafted in three variants : equal installments over the term, interest-only with a balloon at maturity, or single lump sum at maturity. The amortization table is generated automatically from the principal, rate, and term you enter.

- The default and acceleration clauses define what constitutes a default (typically a missed payment unremedied for 10 to 30 days, plus death, insolvency, or material misrepresentation by the maker) and grant the holder the right to declare the entire unpaid balance immediately due. Without acceleration, the lender must sue installment by installment as each one comes due, an expensive and slow process.

- The cosigner block binds a second person jointly and severally for the full obligation under §3-419 UCC (accommodation party). The cosigner signs the note itself, not a separate guarantee, so the obligation rides with the instrument if it is ever transferred.

- The prepayment, late fees, attorneys' fees and choice-of-law clauses complete the package. Late fees are capped at the state maximum (typically 5 % of the missed payment in most states). Attorneys' fees are recoverable only if the note says so explicitly, and the choice-of-law clause designates the lender's home state, subject to mandatory consumer-protection rules in the borrower's state.

State-specific considerations

Federal law sets the floor ; state law sets the rate, the form, and the collection process. The differences are large enough that copying a California note into a New York transaction can void the interest entirely.

California. Non-exempt personal loans are capped at 10 % per year on unpaid principal under Cal. Civ. Code §1916-1, with broad exemptions for licensed lenders. The statute of limitations on a written note is four years under Cal. Code Civ. Proc. §337, shorter than the UCC default and a frequent trap. California also requires a Consumer Loan Law license for any lender making more than five consumer loans in a 12-month period, which catches some informal lenders by surprise.

Texas. Tex. Fin. Code §302.001 sets the default rate at 6 % per year when the writing is silent, and allows up to 10 % when the parties contract for it. Higher tiers (up to 18 % on consumer loans, higher for commercial) require statutory disclosures. The Texas statute of limitations on a written note is four years from accrual under Tex. Civ. Prac. & Rem. Code §16.004. Texas also enforces the homestead protections of Tex. Const. Art. XVI §50, which limit the use of a primary residence as collateral.

Florida. §687.03 Fla. Stat. caps interest at 18 % on loans under $500,000 and 25 % on larger loans. Charging above 25 % is criminal usury under §687.071. Florida applies a five-year statute of limitations to notes under §95.11(2)(b), slightly longer than California and Texas. Florida courts strictly enforce the usury cap : a single overage can void all interest, and willful violations can void the principal too.

New York. N.Y. Gen. Oblig. Law §5-501 caps civil usury at 16 %, and N.Y. Penal Law §190.40 criminalizes rates above 25 %. New York's statute of limitations on a written contract is six years under CPLR §213. New York courts are particularly aggressive on usury : the Adar Bays v. GeneSYS decision made any loan above the criminal cap void ab initio, principal included, even when the borrower is a sophisticated business. Any note where one party is in New York deserves a careful usury review before signing.

How to fill out this promissory note

The flow on Captain.Legal is built to keep you out of the most common drafting traps without making you read the statute book. You start by selecting the lender's home state, which sets the default interest cap, the statutory rate for the fallback clause, the late fee maximum, and the local statute of limitations. The form then asks for the parties' legal names and addresses as shown on government-issued ID, and prompts you to confirm marital status in community-property states so the spousal disclaimer can be added if needed.

You then enter the principal amount, the loan date, and the maturity date or installment schedule. The amortization is computed live, so you see the monthly payment, total interest, and final balance before you finalize the document. The interest rate field warns you if you exceed the state usury cap. The default clause, acceleration, prepayment, late fees, and attorneys' fees are presented with sensible defaults that you can adjust clause by clause. If a cosigner is involved, a second signature block opens with the §3-419 accommodation party language pre-loaded. The final step generates a Word and a PDF version, both with execution blocks formatted for in-person or notarized signing. The whole process takes about ten minutes for a typical family loan.

Common mistakes to avoid

The first mistake is rounding the interest rate up to a memorable number without checking the state cap. A 12 % rate sounds reasonable to a lender used to credit-card pricing, but it exceeds the California civil usury cap of 10 % on non-exempt loans and produces an unenforceable interest obligation under Cal. Civ. Code §1916-3. The fix is trivial : check the cap before drafting, and use a usury savings clause as a belt-and-suspenders backup. The second mistake, almost as common, is leaving the maturity date blank or writing "to be agreed". A note without a definite or determinable maturity date is not a negotiable instrument under §3-104(a)(2) UCC. It may still be enforceable as a simple contract, but you have lost the procedural advantages of negotiable status.

The third mistake is failing to keep proof of disbursement. A signed note without a corresponding bank wire, cleared check, or deposit slip invites the failure of consideration defense at trial, where the borrower simply claims the funds were never advanced. Wire the funds, keep the confirmation, and reference the disbursement date in the note itself. The fourth is forgetting to address the cosigner's discharge rights under §3-605 UCC. A holder who modifies the note or releases collateral without the accommodation party's consent can extinguish the cosigner's liability entirely. The release-and-modification waiver in the cosigner block is there for that reason. Finally, do not let the original note disappear : §3-309 UCC lets you sue on a lost note, but the procedure requires a sworn affidavit, posting of indemnity, and significantly more proof than producing the original paper. Store the signed original in a secure location and circulate signed copies only.

Frequently Asked Questions

35 verified reviews · 50 000+ downloads

- Immediate access to the document

- PDF + Word download

- Compliant with 2026 legislation

- Reviewed by lawyers

You might also like