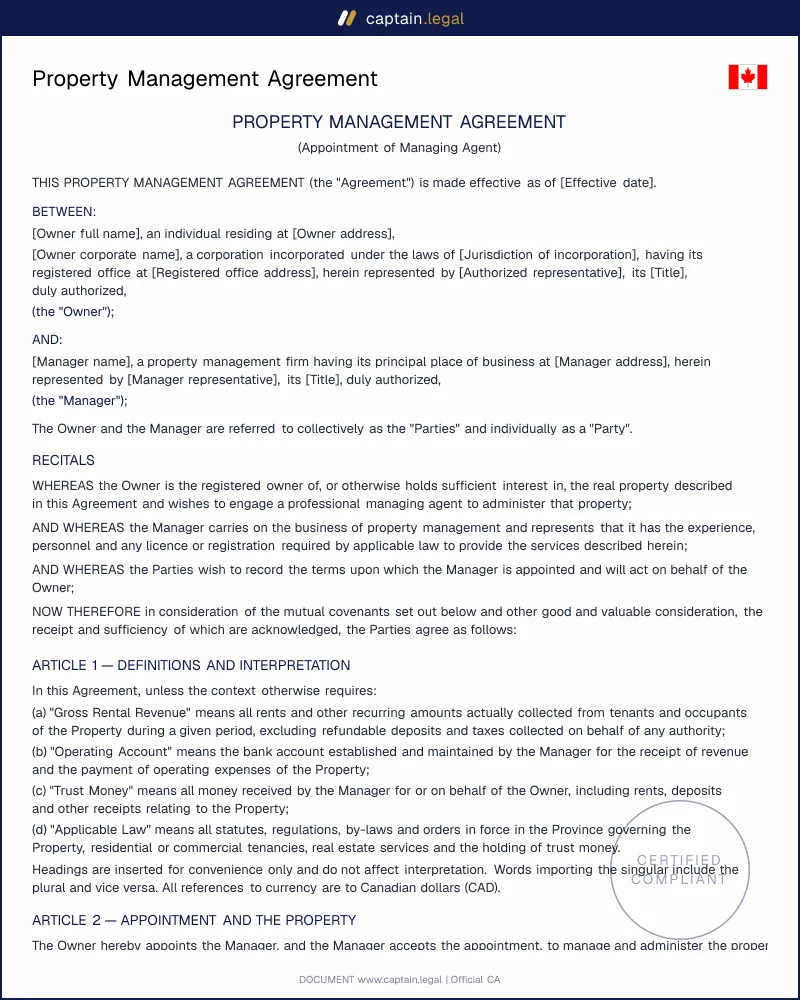

No single federal statute governs property management in Canada. The relationship rests first on the common law of agency and contract, supplemented heavily by provincial legislation that decides, province by province, whether the manager even needs a licence and how it must hold your money. This is the part owners most often miss, and it is where a generic template downloaded from an American site becomes dangerous.

In British Columbia, rental property management for compensation is a licensed activity under the Real Estate Services Act (RESA), administered by the BC Financial Services Authority. Rental property management services there include trading services in relation to the rental of real estate, collecting rents or security deposits, and managing the real estate on behalf of the owner. The statute is strict on structure: an individual manager must work through a licensed brokerage supervised by a managing broker, and there is no sole-practitioner licence. The consequences of getting this wrong are not theoretical. Providing real estate services without the required licence is an offence under section 118 of RESA, and BCFSA enforcement has produced six-figure penalties and disgorgement orders against unlicensed operators. Owners commissioning a manager in BC should confirm the manager's licence and read the Canadian real estate and rental document guide before signing anything.

In Ontario, the regime is different again. The Trust in Real Estate Services Act, 2002 (TRESA) governs brokerages and salespersons who trade in real estate, and the Real Estate Council of Ontario administers it; prior to December 1, 2023, the same legislation was titled the Real Estate and Business Brokers Act, 2002. Residential tenancy itself runs through the Residential Tenancies Act, 2006, which caps deposits and fixes notice periods that a manager must respect. For the statutory text and current licensing position, the authoritative source is the BC Financial Services Authority guidance on rental property management licensing. Across every province, one feature is constant: money the manager collects is held in trust, it is not the manager's to spend, and the agreement must reflect that with a dedicated trust-accounting clause.