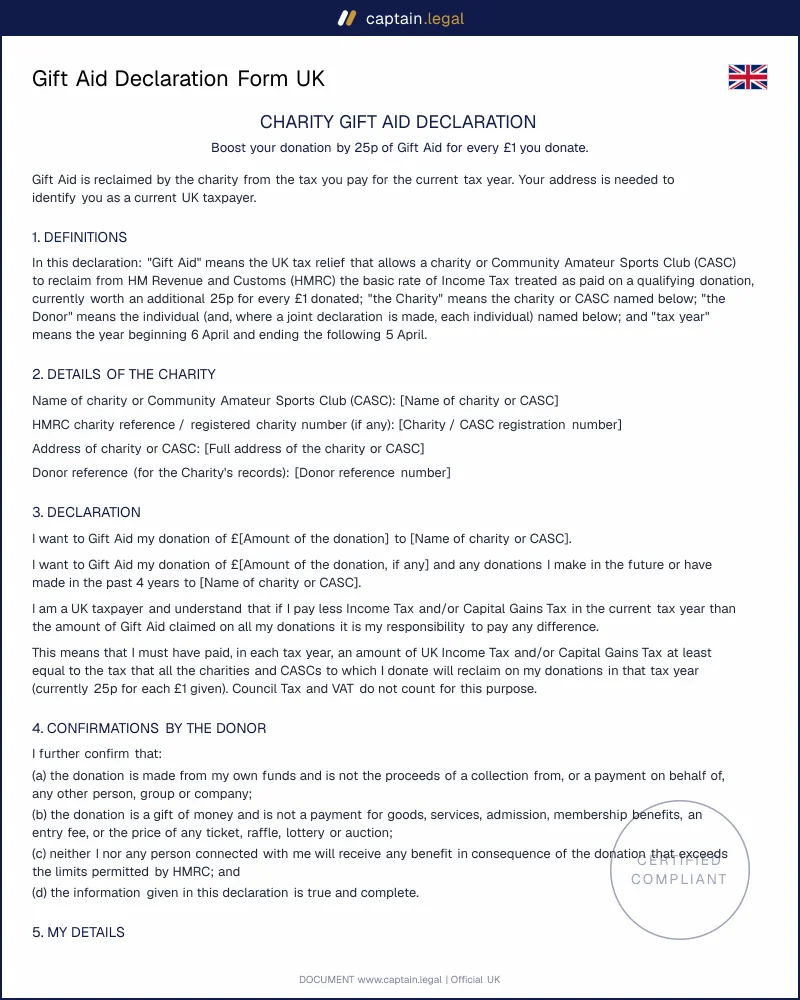

Gift Aid is a UK-wide scheme administered by HMRC, but devolved Income Tax rates create wrinkles worth flagging to donors. For donors resident in England and Northern Ireland, the position is straightforward: the charity reclaims at the UK basic rate, and higher and additional rate taxpayers claim the difference between their rate and basic rate through Self Assessment. Nothing about the declaration form changes by location, and the same wording serves donors across all four nations.

For Scotland, the Scottish Parliament sets its own Income Tax bands under powers in the Scotland Act 2012, yet the charity's reclaim is unaffected: charities still recover Gift Aid at the rest-of-UK basic rate on donations from Scottish taxpayers. The complication is purely at the donor's end. A Scottish taxpayer on the intermediate, higher, advanced or top rate can reclaim the difference between the rate they actually pay and the basic rate the charity has claimed, which means more of your Scottish supporters than you might expect have personal relief to claim back. The declaration itself needs no Scottish variant.

For Wales, Welsh rates of Income Tax apply, but the outcome mirrors Scotland in the way that matters to charities: Gift Aid continues to be reclaimed at the UK basic rate, and Welsh donors paying above it can claim the difference. Across every nation the practical message to put to donors is the same: the form works identically wherever they live, and any higher-rate relief is theirs to pursue personally. Charities employing staff alongside fundraising will find our UK employment contract and HR templates a useful companion set.