Annual general meeting minutes are the formal record of a UK charity's most consequential governance event of the year, the moment when members or trustees approve the accounts, reappoint the board, and ratify the decisions that auditors and the Charity Commission will scrutinise in the months that follow. Drafted well, AGM minutes are a calm, evidential document that protects trustees personally and keeps the charity in good regulatory standing. Drafted poorly, they are the reason a grant is refused or a regulatory case is opened. This AGM minutes template is built for charitable incorporated organisations, unincorporated charities and charitable companies registered in England and Wales, with drafting notes for trustees in Scotland and Northern Ireland.

Compliant

2026 Legislation

50,000+ clients

trust us

Affordable

From $4.90 / doc

Secure payment

Instant download

UK Charity AGM Minutes Template | Word & PDF, Lawyer-Drafted

Secure payment · No subscription

What are AGM minutes?

AGM minutes are the contemporaneous written record of a charity's annual general meeting, signed by the chair and kept with the charity's statutory records. They differ from ordinary trustee meeting minutes in three important ways: the AGM is convened on formal notice to the charity's members where members exist, it follows an agenda fixed by the governing document, and its decisions include the approval of the Trustees' Annual Report and accounts together with the election or re-election of trustees. For charities without a membership structure, such as CIO Foundations or family-trust charities, the AGM is held by the trustee body itself and serves much the same evidential purpose.

The minutes are not a verbatim transcript. They capture what was decided, who proposed and seconded each motion, how the vote went, and any conflicts that were declared and managed. A common confusion concerns the distinction between AGM minutes and extraordinary general meeting (EGM) minutes: an EGM is a meeting called between AGMs to deal with a single urgent issue, typically a constitutional amendment, the removal of a trustee, or an unscheduled financial matter. Both documents follow the same drafting discipline, but only the AGM minutes form part of the annual governance cycle required by the charity's constitution and, where applicable, by the Charities Act 2011. If your governing document says the AGM must be held by a specific date each year, that deadline is binding.

Legal framework

For charities registered in England and Wales, the obligation to keep AGM minutes flows from a combination of the Charities Act 2011, the charity's own governing document, and Charity Commission guidance. The Commission's foundational publication, The essential trustee: what you need to know, what you need to do (CC3), treats accurate meeting records as central to the personal duties that trustees discharge. CIOs are additionally governed by The Charitable Incorporated Organisations (General) Regulations 2012, which prescribe specific record-keeping requirements for member decisions, including written resolutions taken outside meetings.

Charitable companies limited by guarantee must comply with sections 355 to 359 of the Companies Act 2006. Minutes of every general meeting have to be kept for at least ten years and made available for inspection by members, and they are formally evidence of the proceedings under section 357. This is why charitable companies typically run their AGM with the same procedural rigour as commercial companies apply to their UK company board minutes and shareholder records; the wording differs but the evidential test is the same.

The Commission expects every charity to produce a Trustees' Annual Report and accounts each financial year, with the threshold for independent examination or full audit set by section 144 of the Charities Act 2011. AGM minutes are the formal record that those accounts were considered and approved by the membership or the board, and they are routinely requested during a regulatory review or grant due diligence.

Outside England and Wales, the position differs. Scottish charities are regulated by the Office of the Scottish Charity Regulator (OSCR) under the Charities and Trustee Investment (Scotland) Act 2005. Charities in Northern Ireland answer to the Charity Commission for Northern Ireland (CCNI) under the Charities Act (Northern Ireland) 2008. Trustees operating across borders should confirm their primary regulator before finalising the AGM minutes.

When do you need this document?

The most obvious trigger is the annual cycle imposed by the governing document. Most charity constitutions require an AGM to be held within a specified window after the financial year-end, often six months or earlier, and the trustees breach their own constitution the moment that deadline slips without explanation. A short delay can usually be cured by a written note in the next minutes, but a habit of missed AGMs is the kind of pattern that funders and the Charity Commission notice quickly.

You also need this document whenever the charity is approving the annual accounts or the Trustees' Annual Report. The approval has to be visible in the minutes, ideally as a recorded resolution naming the document by date and including the financial year-end. The same applies to the appointment of an independent examiner or auditor, the re-election or rotation of trustees under the constitution, and the adoption of any constitutional amendments that the governing document reserves to the members.

Two edge cases are worth flagging. The first is the purely virtual AGM: legally permissible in most modern charity constitutions, but the minutes must record the technology used, how quorum was verified online, and how voting was conducted. The second is the AGM of a small charity with no members other than the trustees themselves, common among CIO Foundations and family-trust charities. The meeting still happens; the minutes are still required; the formality is not reduced just because the same people wear two hats. Our UK CIO constitution template is drafted with both Association and Foundation models in mind, and the AGM minutes here are calibrated to fit either.

Key clauses included in our template

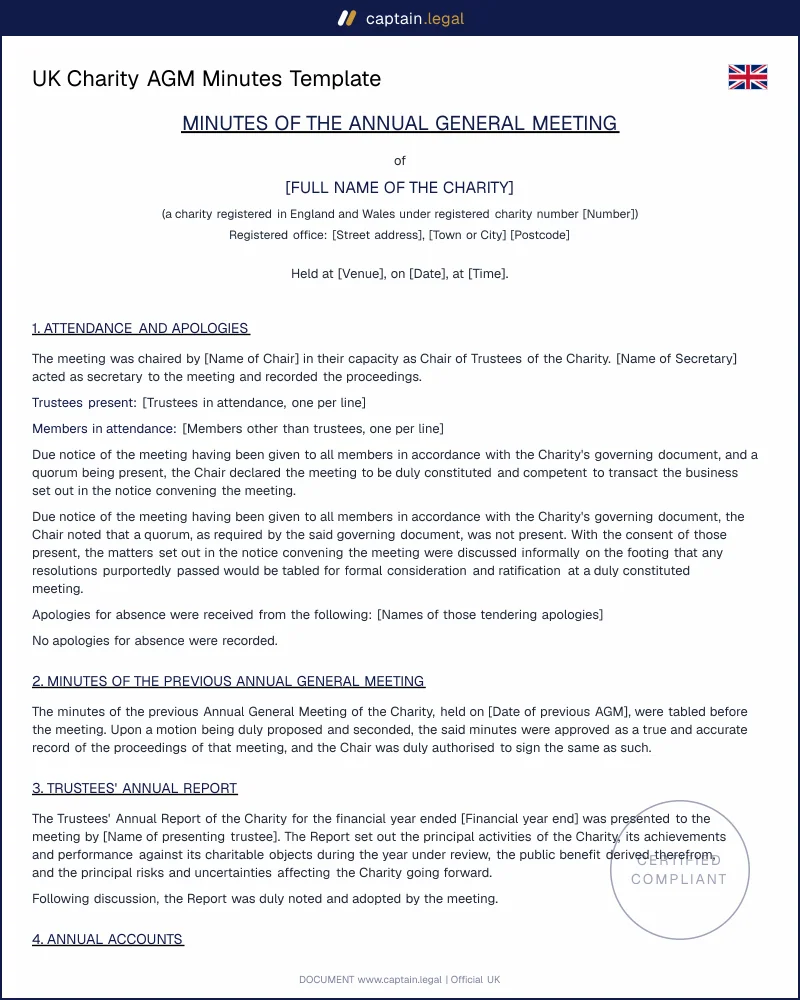

- The notice of meeting and convening section records when and how notice was given to members, the agenda items circulated, and the supporting documents (accounts, Trustees' Annual Report, list of trustees standing for re-election). This is the first item a regulator or auditor checks if the validity of the AGM is later questioned.

- The quorum verification clause captures the number of members present in person and electronically, set against the quorum threshold in the governing document. A meeting held without quorum produces no binding decisions, however well-attended it otherwise was. The template prompts the chair to record the precise time quorum was reached.

- The approval of previous AGM minutes confirms that last year's record has been accepted as a true reflection of what was decided. Any corrections are noted, and the minutes are then signed by the current chair, closing the loop on the previous year's governance and protecting it against later challenge.

- The Trustees' Annual Report and accounts resolution records approval of the financial statements for the year, naming the period and the independent examiner or auditor where appointed. The wording follows the format expected under section 144 of the Charities Act 2011 and ties directly into the charity's annual return.

- The trustee elections and re-elections clause captures nominations, seconders, the vote, and the term of office for each appointment. Where the constitution staggers rotation, the template prompts the secretary to record which seats are in rotation that year, with their replacements.

- The any other business and closing block records any matters formally raised, the date of the next AGM, and the chair's signature. Items that should have been on the agenda but were not formally notified are flagged rather than buried, which protects the validity of the decisions taken and aligns with the discipline expected across our wider UK charity governance templates.

How to fill out the AGM minutes

You start by telling our wizard which form of charity you operate: a CIO with members, a CIO Foundation, a charitable company limited by guarantee, or an unincorporated association. The template loads the appropriate constitutional references and adjusts the resolution wording accordingly. From there, you enter the date, venue (or video-conferencing platform) and the financial year just ended, and the document numbers itself in the format auditors expect.

The next stage handles attendance. You list the trustees present, the members present in person or electronically, any apologies received in writing, and any non-members in attendance such as the independent examiner or solicitor. The wizard then asks whether quorum was confirmed and at what time, and produces the recorded statement automatically.

The substantive part of the minutes is built clause by clause: approval of previous minutes, presentation and approval of the Trustees' Annual Report and accounts, re-appointment of the independent examiner, election or rotation of trustees, and any special resolutions. Each item invites you to record the proposer, seconder, votes for and against, abstentions, and any declared conflicts. Charities that hold real estate as part of their assets are often asked to ratify a lease, licence or property disposal at the AGM, and the supporting paperwork can be drawn from our UK real estate document templates. Once complete, the minutes are exported in Word and PDF, ready for circulation to members and storage in the charity's statutory records.

Common mistakes to avoid

The most frequent failure has nothing to do with the meeting itself: it is insufficient notice. Constitutions typically require fourteen or twenty-one clear days' written notice to members, and the calculation excludes the day of service and the day of the meeting. A chair who issues notice on the wrong calendar basis discovers the problem only after a member challenges a resolution, and the entire AGM may need to be redone. Equally damaging is the failure to verify quorum at the moment of decision, not just at the start. Members drop off virtual meetings; if the recorded vote happens after quorum has slipped, the resolution is vulnerable.

The next category is poor minute discipline. Vague decision wording such as "the trustees agreed to proceed" tells you nothing about what was agreed, on what evidence, or whether a vote was taken. Conflicts of interest cause repeated problems when they are mentioned but not visibly managed: the template prompts the secretary to record the declaration, the trustee leaving the meeting, the remaining quorum, and the substantive decision. A related trap concerns decisions about staff or workplace policy taken at the AGM without the proper underlying paperwork; if your charity employs anyone, the right UK employment and HR document templates need to sit underneath any AGM-level approval. Finally, minutes drafted but never signed are minutes that no auditor or court will rely on. The chair's signature, dated, is what converts the draft into evidence.

Frequently Asked Questions

21 verified reviews · 50 000+ downloads

- Immediate access to the document

- PDF + Word download

- Compliant with 2026 legislation

- Reviewed by lawyers

You might also like