A Limited Liability Partnership Agreement is the private constitution that governs how an LLP incorporated under the Limited Liability Partnerships Act 2000 actually operates. Companies House registers the LLP and publishes its members, but it never sees this agreement, and that is precisely the point. Without one, your LLP defaults to the eleven default rules set out in the Limited Liability Partnerships Regulations 2001 — equal profit shares, equal management rights, no power to expel a member, and no mechanism to deal with retirement or death. For any partnership of solicitors, accountants, surveyors, consultants, architects or property investors, those defaults are unworkable. A properly drafted LLP agreement replaces them with a bespoke deal between members.

This template is drafted to the standard expected by a London commercial firm. It covers capital contributions, profit-sharing waterfalls, drawings, decision-making thresholds, designated members' duties, exit and compulsory retirement, restrictive covenants and dispute resolution, all anchored to the LLP Act 2000 and the Companies Act 2006 provisions that apply to LLPs by reference.

Compliant

2026 Legislation

50,000+ clients

trust us

Affordable

From $4.90 / doc

Secure payment

Instant download

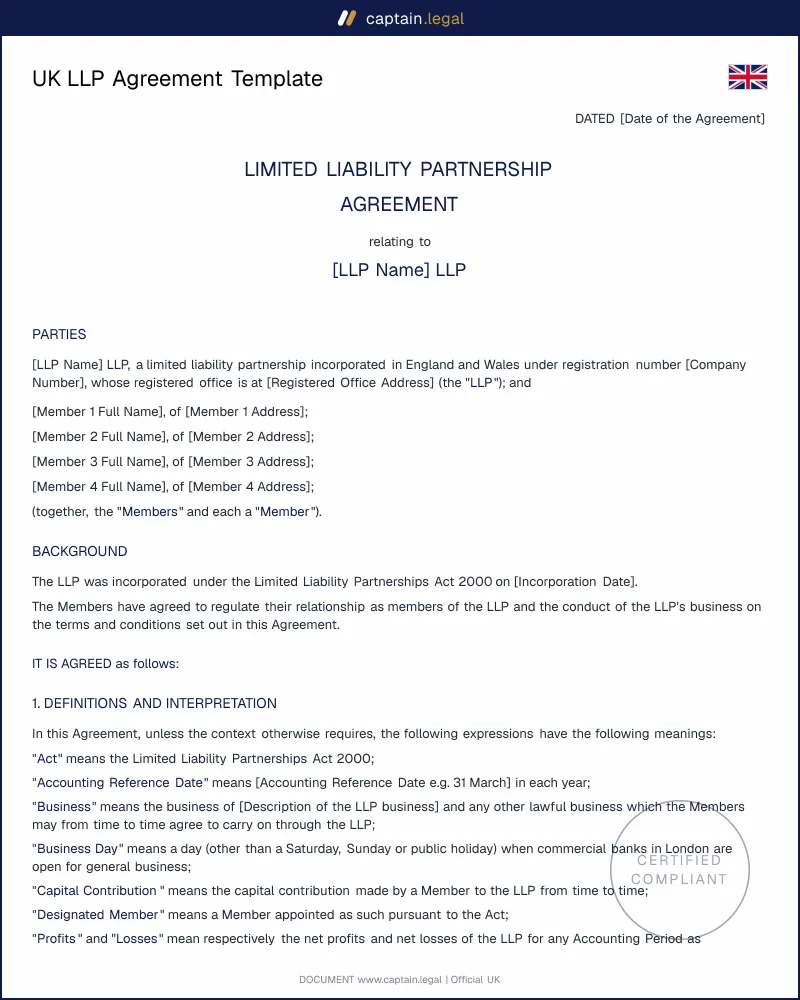

UK LLP Agreement Template | Override the Default LLP Rules

Secure payment

What is a Limited Liability Partnership Agreement?

The LLP agreement (also called the members' agreement or deed of partnership) is a private contract between the members of a Limited Liability Partnership. It is not filed at Companies House and never becomes a public document, which is why members can negotiate commercially sensitive terms — profit splits, capital ratios, garden leave, non-competes — without exposing them to clients or competitors.

Practitioners often confuse three instruments that look similar but do entirely different jobs. A traditional partnership agreement governs an unincorporated partnership under the Partnership Act 1890 and gives each partner unlimited personal liability for the firm's debts. Articles of association, by contrast, are the constitutional document of a limited company under the Companies Act 2006 and are publicly filed. The LLP agreement sits between the two. It governs a body corporate with separate legal personality and limited liability for its members under section 1(2) of the LLP Act 2000, but it is structured contractually like a partnership rather than constitutionally like a company. The members are taxed personally on their share of profits, the LLP itself is transparent for income tax, and the internal mechanics — quorum, voting, expulsion, capital — are entirely a matter of private agreement. If your LLP has no written agreement, the eleven default regulations apply by operation of law, and they are almost never what the founding members intended. Drafting the agreement before the LLP starts trading is the only sensible sequence.

Legal framework

The LLP is a creature of statute. The Limited Liability Partnerships Act 2000 established the body corporate, conferred separate legal personality at section 1(2), and limited members' liability to the amount they have agreed to contribute. The Limited Liability Partnerships Regulations 2001 (SI 2001/1090), as amended by the Limited Liability Partnerships (Application of Companies Act 2006) Regulations 2009 (SI 2009/1804), import a substantial portion of the Companies Act 2006 into LLP law: accounts and audit, registered office, charges, insolvency and disqualification of members all flow from the Companies Act with appropriate modifications. The official text of the LLP Act 2000 published on legislation.gov.uk is the primary source every drafter should keep open.

Two regulations matter most when the agreement itself is silent. The default rules in regulation 7 of the 2001 Regulations cover profit sharing, indemnity, management participation, books and records, expulsion and assignment of interest. Regulation 8 deals with rights on cessation of membership. Both are residual: any clear contrary provision in the LLP agreement displaces them. Practitioners should never rely on partial coverage — drafting silence on retirement, for example, leaves you with a member you cannot lawfully expel because regulation 7(8) provides that no majority of members can expel another member without express agreement.

The agreement must be executed as a deed if it includes covenants intended to be enforceable beyond the limitation period for simple contracts, or if any member is contributing property requiring a deed of transfer. Execution as a deed under the Law of Property (Miscellaneous Provisions) Act 1989 requires the document to be signed in the presence of a witness who attests the signature. Stamp Duty Land Tax may apply where a member contributes UK real estate to the LLP, and HMRC's Statement of Practice D12 governs the tax treatment of capital movements between members. The LLP must also file an LL IN01 form at Companies House at incorporation and notify any change of members on form LL AP01 or LL TM01. For founders comparing structures before incorporation, our overview of UK business legal documents sets out where the LLP fits alongside companies and sole traderships.

When do you need this document?

The most frequent trigger is the moment two or more individuals agree to set up a professional services firm together. Solicitors, chartered accountants, chartered surveyors, architects, dental practices and increasingly tech consultancies favour the LLP because it ringfences personal assets from professional negligence claims while preserving partnership-style profit allocation. The agreement should be in place on or before the date the LLP begins to trade, not bolted on six months later when the first commercial dispute arises. Members who delay routinely discover that the default regulations have been silently governing their relationship in a way none of them would have accepted on day one.

A second classic scenario is conversion. An existing general partnership under the Partnership Act 1890 decides to convert to an LLP for liability reasons. The LLP agreement here typically mirrors the existing partnership deed clause by clause, but updated to reflect the new statutory framework, the abolition of joint and several liability for ordinary debts, and the new designated members' regime. Property partnerships moving to LLP form to hold investment portfolios also need bespoke clauses on capital accounts and CGT-sensitive distributions ; our UK real estate legal templates cover the leasehold and freehold paperwork that typically accompanies such restructurings.

The third use case is the admission of a new equity member to an existing LLP. The original agreement should anticipate this with a deed of accession, but where it does not, the existing members must execute a fresh agreement or a deed of variation. Edge case worth flagging: an LLP with only two members where one dies or retires must admit a new member within six months, otherwise section 4A of the LLP Act 2000 triggers personal liability for the surviving member from the seventh month onwards. A retirement clause that fails to address this scenario is not a complete agreement.

Key clauses included in our template

The template runs to roughly forty clauses and four schedules. The drafting reflects how a London commercial firm would structure a partnership of equals, with adjustments available for fixed-share members and salaried members.

- The capital contributions schedule records each member's initial capital, the form it takes (cash, real property, intellectual property, goodwill), and the agreed valuation date. It distinguishes capital from current account balances, because the LLP Regulations 2001 treat them very differently on cessation of membership and the distinction also drives the capital allowances available to each member.

- The profit-sharing and drawings clauses set out the order of priority: first interest on capital, then fixed profit shares for fixed-share members, then a discretionary pool, and finally the residual equity allocation between full members. The clause specifies monthly drawings against anticipated profit, the year-end true-up mechanism, and a clawback for members who have over-drawn relative to actual results.

- The decision-making framework distinguishes ordinary matters (simple majority of members), reserved matters (special majority of 75 % by profit share), and unanimous matters such as admission of a new member or amendment of the agreement itself. Quorum requirements and notice periods for members' meetings are aligned with the Companies Act 2006 practice imported by the 2009 Regulations.

- The designated members' provisions identify which members carry the statutory duties under section 8 of the LLP Act 2000: signing the accounts, filing the annual confirmation statement, notifying Companies House of changes, and acting as the administrative interface with the registrar. An LLP must have at least two designated members at all times, and if no member is designated, every member is treated as designated by default.

- The restrictive covenants cover non-compete, non-solicitation of clients and staff, and confidentiality during membership and for a defined period after departure. The covenants are drafted to the Tillman v Egon Zehnder standard set by the Supreme Court and are explicitly severable.

- The exit and compulsory retirement clauses govern voluntary retirement notice, retirement on grounds of incapacity, expulsion for cause, and the buy-out formula applicable to the departing member's capital and current account. A good leaver / bad leaver mechanism adjusts the goodwill component of the exit valuation.

Regional and sectoral considerations

England, Wales, Scotland and Northern Ireland share the same LLP Act 2000, but practical drafting points diverge along sectoral and regulatory lines.

Solicitors' LLPs must comply with the SRA's Authorisation Rules and the Code of Conduct for Firms. The agreement needs an explicit clause confirming that the LLP is a recognised body under section 9 of the Administration of Justice Act 1985, that compliance officers (the COLP and COFA) are designated as such within the membership, and that any member's misconduct triggering an SRA intervention is treated as automatic grounds for expulsion. The SRA Accounts Rules on client money also have to be reflected in the books and records clause.

Accountancy and audit LLPs operate under the ICAEW or ACCA regulatory regime. The agreement should require members to maintain professional indemnity insurance to the firm's prescribed minimum and should empower the management committee to suspend a member whose practising certificate is withdrawn. Engagement letters and audit engagement clauses under ISA 210 also influence the way members' liability inter se is allocated, and the agreement typically carves out audit-related claims from the indemnity given by the LLP to its members.

Property investment LLPs holding UK real estate face Stamp Duty Land Tax exposure on member changes if the property has been contributed within the previous three years. The agreement should record the capital contribution as a property contribution, attach the deed of contribution as a schedule, and align with HMRC's SDLT manual paragraph 33000 on partnership transactions. Where the property generates rental income, the profit allocation clause should be drafted to follow the underlying tax transparency, not to override it.

Scottish LLPs are subject to Scots law on partnership and on the execution of deeds. Execution requires either two witnesses or self-proving status under the Requirements of Writing (Scotland) Act 1995. The dispute resolution clause should be drafted with the Court of Session jurisdiction and Scots law of contract in mind rather than English law, otherwise enforcement in Edinburgh will face an immediate jurisdictional objection.

How to fill out this LLP agreement

The Captain.Legal flow opens with the basic identity questions: the proposed name of the LLP, the registered office address, and the names and addresses of the founding members. From there, the form branches according to whether the LLP has been incorporated yet at Companies House. If the LLP already has an OC number, you enter it ; if not, the agreement is drafted as a pre-incorporation deed conditional on registration. The next block addresses capital. You allocate the initial contribution of each member, choose between fixed-share, salaried, and full equity status for each, and specify the profit-sharing percentages. The form runs an internal check that the percentages reconcile to 100 % before letting you continue.

Decision-making thresholds come next. You select which matters are ordinary, reserved, or unanimous, and the form pre-loads sensible defaults you can override clause by clause. Restrictive covenants are then configured by sector — legal, accountancy, consulting, property, technology — with the post-termination period adjustable between six and twenty-four months. Designated members are picked from the member list, with a hard requirement of at least two. Finally, the agreement is generated as Word and PDF, ready for execution as a deed in the presence of witnesses. For HR-side documents that frequently accompany LLP setups, our UK employment contracts and HR templates cover salaried members' service agreements and consultant engagements.

Common mistakes to avoid

The most damaging error is silence. Members who sign a one-page founders' note and assume the LLP Act covers the rest find out the hard way that the default rules in regulation 7 give every member equal voting rights regardless of capital, prohibit expulsion without unanimity, and entitle a retiring member to nothing beyond return of capital. A properly drafted exit clause changes all three outcomes, but only if it is in the agreement before the dispute starts. A second frequent mistake is treating the LLP as if it were a limited company, importing share-class language and pre-emption rights that have no analogue in LLP law and that conflict with the contractual structure of membership interests.

A third trap concerns designated members. Founders often nominate one designated member only, then forget to update Companies House when that person leaves, exposing the remaining members to personal liability for filing failures under section 8(4) of the LLP Act 2000. The agreement should automate succession of the designated member role on cessation. Practitioners also routinely under-draft the non-compete and non-solicitation clauses, copying language from employment contracts that fails the reasonableness test when applied to a senior LLP member with a profit share. The covenants must be calibrated to the seniority and profit share of the departing member, not lifted wholesale from a junior employee handbook. Finally, agreements drafted without thought to insolvency — particularly the clawback provisions under section 214A of the Insolvency Act 1986, which can require members to repay drawings made within two years of an insolvent winding-up — leave members exposed to liabilities they assumed the LLP shielded them from.

Frequently Asked Questions

24 verified reviews · 50 000+ downloads

- Immediate access to the document

- PDF + Word download

- Compliant with 2026 legislation

- Reviewed by lawyers

You might also like