A statement of capital is the formal snapshot of a UK limited company's issued share capital that sits at the heart of every Companies House incorporation file. It records the total number of shares allotted on formation, the aggregate nominal value, the amount paid up and unpaid on each share, and the prescribed particulars attached to each class of share. For private companies limited by shares, the statement is not a stand-alone filing : it is integrated into Form IN01 alongside the memorandum of association, the articles, and the statement of proposed officers. Get it wrong on day one and the consequences cascade through every confirmation statement, allotment, buy-back and reduction of capital that follows. This page walks you through what the statement contains under section 10 of the Companies Act 2006, when an updated version is required, and how to draft one that survives scrutiny by Companies House and by future investors during due diligence.

Compliant

2026 Legislation

50,000+ clients

trust us

Affordable

From $4.90 / doc

Secure payment

Instant download

UK Statement of Capital Template — Companies Act 2006 (IN01)

Secure payment

What is a statement of capital?

A statement of capital is the document, mandated by sections 9 and 10 of the Companies Act 2006, that records the issued share capital of a company limited by shares at a given date. It replaced the old concept of authorised share capital on 1 October 2009, the day the bulk of the 2006 Act came into force. Before that reform, every company's memorandum had to fix a ceiling on the shares it could issue, and that ceiling could only be raised by ordinary resolution. The statement of capital does the opposite job : it photographs what has actually been issued, and it is updated whenever that picture changes.

The document has two distinct lives. The first is at incorporation, where it forms part of Form IN01 and the broader UK company formation paperwork lodged with Companies House. The second is operational : an updated statement of capital must be filed every time shares are allotted, redenominated, consolidated, sub-divided, redeemed or bought back, and it sits inside the annual confirmation statement (Form CS01) whenever the share capital position has shifted since the last filing. The statement is a living instrument, not a one-off declaration, and that distinction trips up directors who treat the IN01 entry as the end of the matter.

People sometimes confuse the statement of capital with the register of members or with a share certificate. They are not the same. The register of members is held internally by the company and lists who owns what ; the share certificate is issued to each shareholder as evidence of title ; the statement of capital is the public-facing aggregate that lives on the Companies House register and is freely searchable by lenders, suppliers and counterparties.

Legal framework

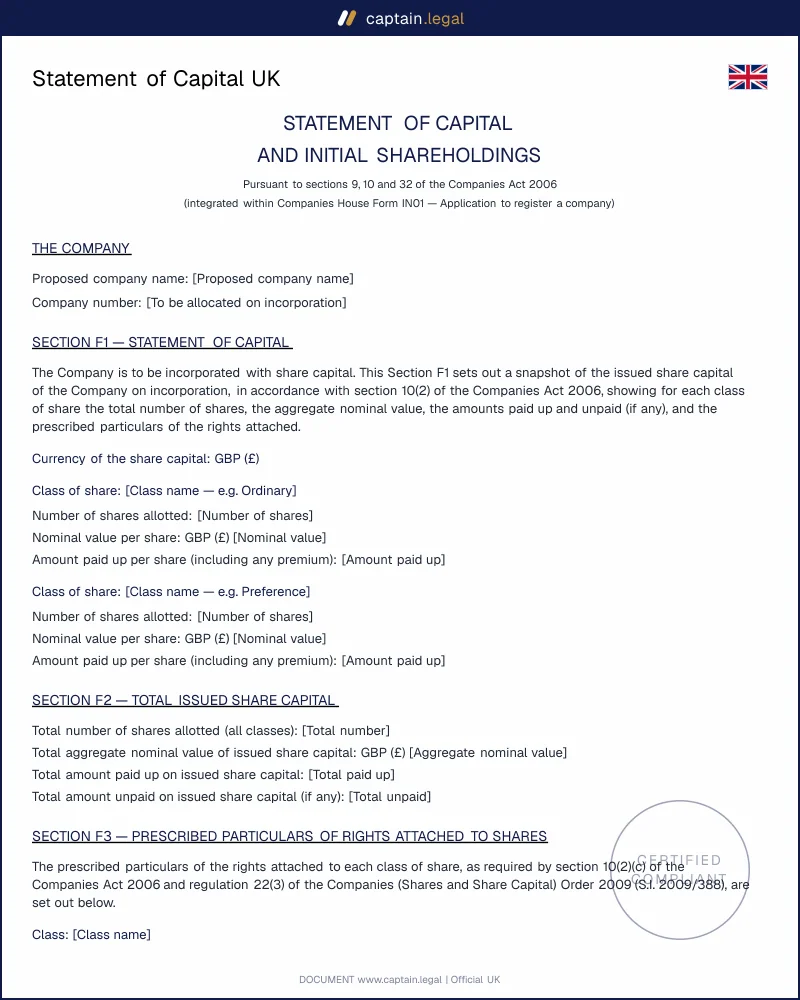

The statutory basis sits squarely in Part 2 of the Companies Act 2006. Section 9 lists the documents that must accompany an application for registration, and section 10 prescribes exactly what the statement of capital and initial shareholdings must contain for any company that is to have a share capital. The required content is precise : the total number of shares to be taken on formation by the subscribers to the memorandum, their aggregate nominal value, any premium payable, the amount unpaid on those shares (whether on account of nominal value or premium), and a breakdown by class of share with the prescribed particulars attached to each class. The prescribed particulars are themselves set out in regulations and cover voting rights, dividend entitlements, capital rights on a winding-up, and redemption terms. You can read the consolidated text on the legislation.gov.uk version of Companies Act 2006 section 10, which remains the authoritative source.

The framework was rewired by the Economic Crime and Corporate Transparency Act 2023 (ECCTA), the most far-reaching set of changes to UK company law since 1844. ECCTA does not alter the substance of the statement of capital itself, but it transforms the environment in which it is filed. Since 18 November 2025, identity verification has been compulsory for all new directors and persons with significant control on incorporation, which means the IN01 carrying your statement of capital will only be accepted once every named officer has obtained a verified Companies House personal code. From spring 2026, the identity verification requirement extends to anyone filing documents on a company's behalf, channelled either through verified individuals or through Authorised Corporate Service Providers (ACSPs). An IN01 lodged without verified identifiers is now liable to outright rejection, and a director acting without verification commits a criminal offence under the new sections 167M and 167N of the 2006 Act.

Form is also unforgiving. The statement of capital must be denominated in a single currency per share class (sterling is standard but any currency is permitted), figures must reconcile to the penny across nominal value, paid-up amount and unpaid amount, and the prescribed particulars must be drafted with sufficient specificity to satisfy regulation 22 of the Companies (Shares and Share Capital) Regulations 2009. Loose phrasing such as "ordinary shares with usual rights" is routinely queried.

When do you need this document?

The textbook trigger is incorporation of a private or public company limited by shares, where the statement of capital is generated automatically as a constituent part of the IN01. Founders setting up a new SPV for a property acquisition, a SaaS startup taking its first round of friends-and-family investment, or a freelancer converting from sole trader to limited company all encounter it on day one. In practice, most accountants and formation agents fold the drafting into the wider incorporation pack alongside the model articles and shareholder agreement bundle for UK businesses, which is why the statement of capital is rarely seen in isolation.

The second category is post-incorporation share capital events. Allotment of new shares to a new investor, a bonus issue funded out of reserves, a reduction of capital under sections 641 to 644 using the solvency statement route, a buy-back of shares out of distributable profits, a sub-division or consolidation under section 618, a redenomination from sterling to euros under section 622 : each of these events compels the company to file an updated statement of capital with the registrar within the statutory window, typically 15 days for allotments under section 555. Miss the window and the directors face daily default fines.

The third category is the annual confirmation statement (Form CS01), where the statement of capital is included whenever the company's share capital has changed since the last confirmation. Even a single share allotment to a new joiner triggers an updated capital block, and forgetting to include it is one of the most common late-filing errors picked up on Companies House compliance reviews.

One edge case worth flagging : groups that operate employee share schemes with monthly or quarterly allotments often batch their updates rather than filing after each individual issue, which is permitted only if every batch falls inside its own 15-day window. Sloppy batching is a recurring source of penalties.

Key clauses included in our template

The Captain.Legal statement of capital template is drafted to slot directly into Form IN01 and to track the structure that Companies House software expects. Each block below maps to a numbered field on the form and to a subsection of section 10 of the Companies Act 2006.

- The identification of the company opens the document with the proposed name, the type (private limited by shares, public limited, or société européenne equivalent), and the registered office address. A misalignment between this block and the IN01 cover sheet is the single most frequent cause of formation rejection, particularly when the proposed name uses a sensitive word requiring prior approval.

- The summary of issued share capital states the total number of shares to be taken by the subscribers, the aggregate nominal value across all classes, and the amount paid up versus unpaid on the whole. This is the headline figure that lenders and credit referencing agencies pull from the public register, so the arithmetic must reconcile down to the last penny against the per-class breakdown.

- The per-class breakdown sets out, for each class of share, the class name (Ordinary, Preference, Deferred, A Ordinary, etc.), the number of shares of that class, the nominal value per share, the aggregate nominal value of the class, the amount paid up per share, and the amount unpaid per share. Where a class has been issued at a premium, the premium is recorded in addition to the nominal value, never inside it.

- The prescribed particulars describe the rights attached to each class : voting rights at general meetings, dividend entitlements (cumulative, non-cumulative, fixed-rate or participating), rights to a return of capital on a winding-up, and any redemption terms. Regulation 22 of the Companies (Shares and Share Capital) Regulations 2009 requires these particulars to be set out with enough detail that a reader can reconstruct the economic rights without reference to the articles ; cross-references like "as set out in Article 7" are insufficient on their own.

- The statement of initial shareholdings lists each subscriber to the memorandum, the number of shares each subscriber takes, the class of those shares, and the amount each subscriber pays. For a single-member company, this collapses into one line ; for a founder-team incorporation, it is the field that establishes the cap table on day one and that drives every dilution calculation thereafter.

Regional considerations

The statement of capital is a UK-wide instrument under the Companies Act 2006, but the registry that processes it varies. England and Wales companies file with Companies House Cardiff, which uses Form IN01 with no jurisdictional variation in the capital block. Scotland companies file with Companies House Edinburgh, which accepts the same IN01 but reads it under the lens of Scots property law on share transfers and bona vacantia rules administered by the King's and Lord Treasurer's Remembrancer rather than the Crown's Bona Vacantia Division. The substantive capital requirements are identical, but striking-off and dissolution routes diverge sharply, which becomes relevant the moment a Scottish company holds undistributed share capital at the point of dissolution.

Northern Ireland companies file with Companies House Belfast under the same 2006 Act framework since the unification of UK company law in 2009. The IN01 and the statement of capital are identical in form. Where Northern Ireland diverges is in the Land Registry (Northern Ireland) treatment of company-held property, which means a NI incorporation handling real estate often needs a coordinated review of the capital structure alongside the residential and commercial tenancy templates available for UK property transactions.

For public limited companies wherever incorporated in the UK, the statement of capital must reflect the statutory minimum authorised minimum of £50,000 (or €57,100) under section 763 of the Companies Act 2006, with at least one quarter of the nominal value plus the whole of any premium paid up before the company can do business or borrow. Plc statements of capital are scrutinised more closely by Companies House examiners, and incomplete prescribed particulars are a near-automatic query.

For companies whose shareholders include non-UK residents, the statement of capital itself is unaffected by residence, but the linked PSC statement and the new identity verification regime under ECCTA mean that overseas individuals must complete IDV through a verified ACSP route before the IN01 will be accepted. A Marrakech-based founder incorporating a UK SPV in 2026 cannot file the statement of capital without going through this verification gate first.

How to fill out this statement of capital

You start on Captain.Legal by choosing the company type, because the statement of capital differs slightly between a private company limited by shares and a public limited company subject to the authorised minimum rules. From there, the form asks for the proposed company name, the registered office, and the country of registration (England and Wales, Scotland, or Northern Ireland), which determines which Companies House office processes the file.

The next block builds the share capital piece by piece. You declare each class of share in turn : the class name, the number of shares to be issued on incorporation, the nominal value per share, the currency, and whether the shares are issued at a premium. The form aggregates these inputs automatically and shows you the running total, so you can spot a typo before you commit. For each class, you then complete the prescribed particulars using the structured prompts (voting rights yes or no, dividend mechanics, rights on a winding-up, redemption terms), and the template translates your answers into the statutory wording expected by Companies House.

The third block ties shares to people : you list each subscriber, the number of shares each takes by class, and the amount each pays. The form runs a final reconciliation between the aggregate capital declared and the sum of the initial shareholdings, and refuses to generate the document until the two figures match. This reconciliation step catches the vast majority of rejection-worthy errors before they reach Companies House. Once validated, you download the statement in Word and PDF and either attach it to your IN01 directly or hand it to your formation agent.

Common mistakes to avoid

The single most damaging error is conflating issued capital with authorised capital. The latter no longer exists for companies incorporated under the 2006 Act, and listing a "share capital of £100,000 with 1,000 shares of £1 each issued" reads as a draft from 1985. The statement of capital records only what is actually issued ; if you want headroom for future allotments, you simply allot new shares when the time comes and file the updated statement, with no need for an authorising ceiling.

A second recurring mistake is rounding the paid-up and unpaid amounts so that the per-share figures fail to multiply cleanly into the aggregate. Companies House software runs these checks automatically and rejects filings where, say, 1,000 shares of £1 nominal value are recorded as £999.99 paid up. The fix is to declare every figure to the same number of decimal places and to verify the arithmetic before submission. A third error is silent on the prescribed particulars, where founders write "ordinary shares with usual rights" and assume the model articles will fill the gap. They will not : the particulars must be set out on the face of the statement.

A fourth, increasingly costly mistake under the post-November 2025 regime is filing without identity verification. A statement of capital naming a director or PSC who has not obtained a Companies House personal code is now liable to immediate rejection, and the company commits a criminal offence by holding an unverified director on its board. The fifth and final classic mistake is forgetting to file an updated statement of capital after an allotment : the 15-day window under section 555 runs from the date of allotment, not from the date of the board minute, and missed deadlines accumulate daily default fines that quickly outweigh any saving on professional fees.

Frequently Asked Questions

21 verified reviews · 50 000+ downloads

- Immediate access to the document

- PDF + Word download

- Compliant with 2026 legislation

- Reviewed by lawyers

You might also like