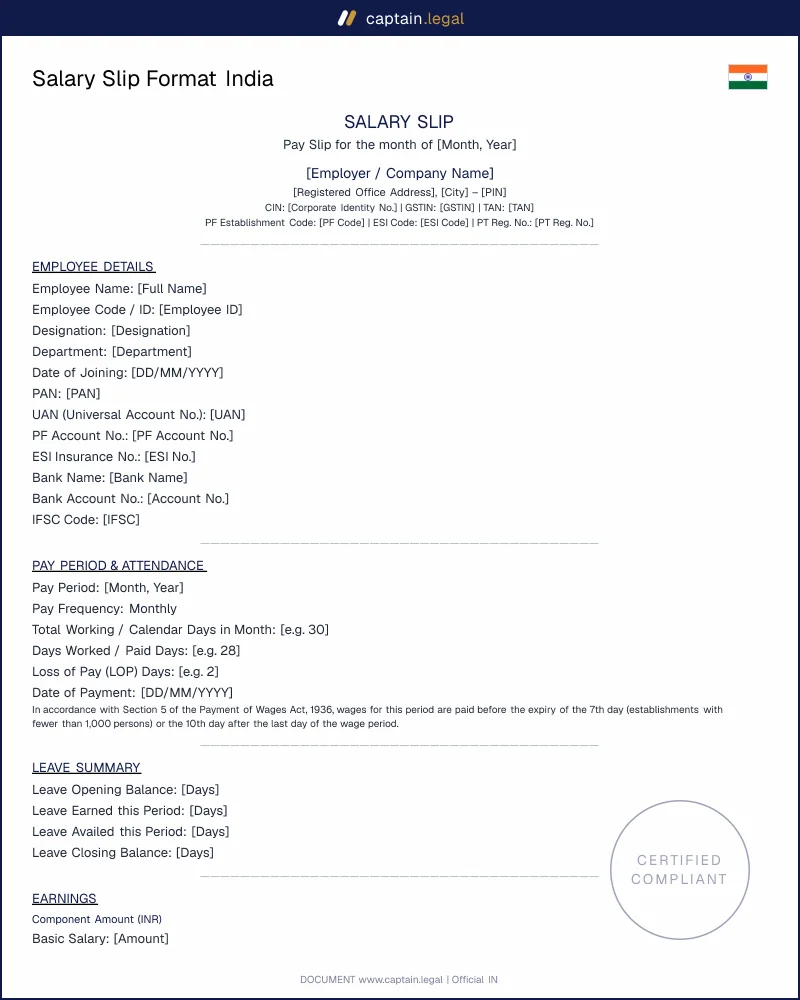

Payslip law in India layers a central code over State-level rules, and the part that varies most by state is Professional Tax, a deduction levied by states rather than the centre.

Maharashtra levies Professional Tax under the Maharashtra State Tax on Professions, Trades, Callings and Employments Act, 1975, with monthly slabs that top out at ₹200 (and ₹300 in the final month of the year for higher earners). A Mumbai or Pune payslip without a PT line is immediately suspect to a local bank, and employers registered under the Maharashtra Shops and Establishments Act must reflect the deduction every month.

Karnataka deducts Professional Tax under its own Profession Tax Act for employees in Bengaluru and across the state, currently exempting lower earners and capping the deduction at ₹200 a month. Given the IT workforce concentration, Bengaluru payslips are among the most heavily scrutinised by visa consulates, so the UAN and PAN fields must be populated correctly.

Tamil Nadu administers Professional Tax through local bodies such as the Greater Chennai Corporation on a half-yearly basis, which means the PT deduction often appears as a larger periodic figure rather than a small monthly one, a difference a Chennai employee should expect to see.

Delhi does not levy Professional Tax at all, so a compliant Delhi payslip will simply omit the PT line, and its presence on a Delhi slip is itself an error. The PF and ESI lines, being central, appear identically across all states.