The governing statute is the Companies Act 2013, read with the Companies (Incorporation) Rules 2014. Section 7 sets out the procedure for incorporation, and Rule 38, introduced in 2016, channels the entire filing through the SPICe+ (INC-32) web form on the MCA portal, where name reservation, DIN allotment, PAN, TAN, EPFO, ESIC and bank account opening are bundled into a single integrated application. For a Private Limited company with up to seven individual subscribers who are Indian residents, the MOA and AOA are not uploaded as separate Word files. They are filed electronically as eMOA (INC-33) and eAOA (INC-34), linked to SPICe+ and digitally signed. Physical attachments are reserved for the exceptions: more than seven subscribers, Section 8 companies, or non-individual first subscribers based outside India, who must attach apostilled MOA and AOA as PDFs.

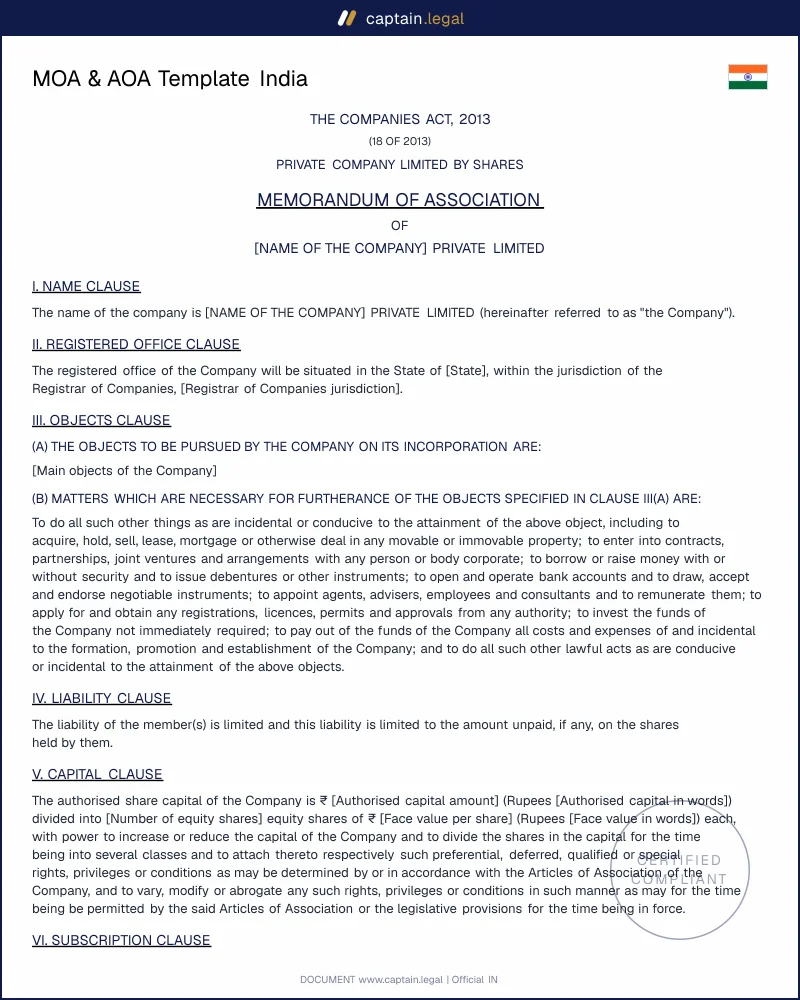

Section 4 dictates the MOA's contents. A point founders still get wrong: the Companies Act 2013 abolished the old three-tier objects structure of the 1956 Act. There is no longer an "other objects" clause. The objects are now stated in two parts only, the main objects the company will pursue on incorporation and the matters considered necessary in furtherance of them. A company can no longer warehouse unrelated future businesses in a catch-all paragraph; activities outside the stated objects require a Section 13 special resolution and a fresh ROC filing. The Companies (Amendment) Act 2015 separately removed the minimum paid-up capital floor, so there is no mandatory capital threshold to incorporate, though you still need at least two shareholders and two directors. The model articles in Table F remain the safe default for a company limited by shares. For the authoritative form and the statutory tables, the Ministry of Corporate Affairs guidance on SPICe+ and the eMOA and eAOA forms is the source that controls ROC practice. If your AOA differs from a separately signed shareholders agreement aligned with the Companies Act 2013, the articles prevail in dealings with third parties, so the two must be reconciled before filing.