The Sole Trader Registration document is the formal record a self-employed individual files with HM Revenue and Customs to start trading legally in the United Kingdom. It is built around a covering letter to HMRC, a Form CWF1 section where applicable, a trading name declaration, and a registration checklist matching the Self Assessment route. The document is drafted for new sole traders, side-hustlers crossing the £1,000 trading allowance, and freelancers transitioning from PAYE-only income. Whether you intend to register online through your Government Gateway account or by post, this sole trader registration template gives you a clean paper trail from day one, which matters when HMRC asks questions two or three years down the line.

Compliant

2026 Legislation

50,000+ clients

trust us

Affordable

From $4.90 / doc

Secure payment

Instant download

Sole Trader Registration UK | Companies Act 2006 & HMRC Compliant

Secure payment

What is a sole trader registration?

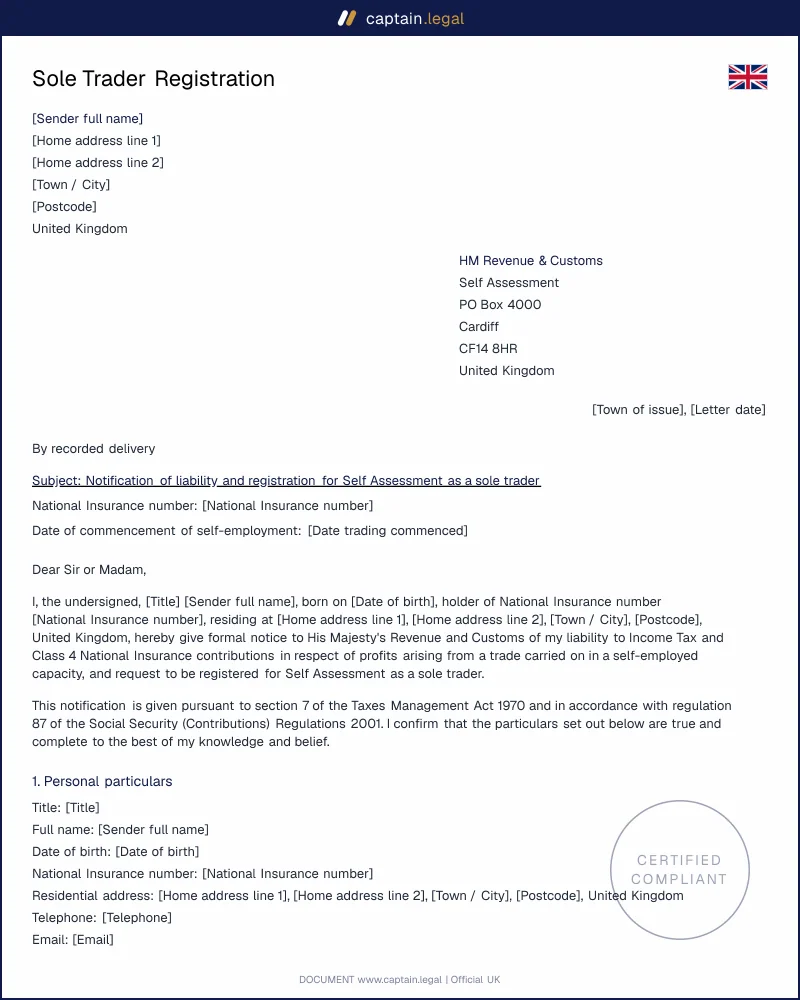

A sole trader registration is the act, and the supporting document, by which a self-employed individual notifies HMRC that they are trading on their own account. The document is not itself a statutory form ; it consolidates what HMRC expects to see, plus the supporting paperwork a sensible practitioner keeps on file. At its core sits the registration request to HMRC, supported by a covering letter identifying you, your trading name, the date you started trading, and the legal basis for registration under the Income Tax (Trading and Other Income) Act 2005.

The document differs from incorporation paperwork in one fundamental way. A sole trader has no separate legal personality : you and the business are one and the same, which is why you register with HMRC for Self Assessment rather than with Companies House under the Companies Act 2006. Limited company founders use entirely different paperwork, including the IN01 application, the memorandum, and bespoke articles of association. By contrast, a sole trader's footprint with the state is much lighter. The trade-off is unlimited personal liability : creditors can pursue your personal assets if the business fails, which is why a clean registration file and a disciplined record-keeping habit from week one are not optional. They are the minimum standard expected by every accountant and every HMRC compliance officer who may eventually look at your books.

Legal framework

The legal architecture for sole trader status in England, Wales, Scotland and Northern Ireland sits across several Acts and a body of HMRC guidance. The duty to notify HMRC of self-employment flows from the Taxes Management Act 1970, section 7, which obliges any person chargeable to income tax or capital gains tax for a tax year to notify HMRC by 5 October following the end of that tax year. For sole traders this is the registration deadline : if you start trading in the 2025-2026 tax year, you must register by 5 October 2026, and missing this date can trigger a "failure to notify" penalty calibrated to the tax at risk under Schedule 41 of the Finance Act 2008. The penalty is potentially-lost-revenue based, so even small unregistered traders are exposed.

Above the £1,000 trading allowance set by the Finance (No. 2) Act 2017, registration is mandatory. Below it, registration is optional but often desirable to claim losses, build a National Insurance record, and establish a credible commencement date. Income tax follows the bands set in the Income Tax Act 2007, and Class 2 and Class 4 National Insurance contributions are collected through Self Assessment under the Social Security Contributions and Benefits Act 1992. VAT registration becomes compulsory once taxable turnover exceeds £90,000 in any rolling twelve-month period under the Value Added Tax Act 1994. From April 2026, Making Tax Digital for Income Tax Self Assessment phases in for sole traders with qualifying income above defined thresholds, requiring quarterly digital updates rather than a single annual return. The official starting point for the registration journey is the HMRC guidance on becoming a sole trader and registering for Self Assessment, which sets out the online and postal routes, the information required, and the Form CWF1 used by individuals already inside the Self Assessment system. Across our UK business document templates, the registration document is the natural first step before any commercial paperwork.

When do you need this document?

The most frequent trigger is the first £1,000 of self-employed income in a tax year. The trading allowance is calculated on gross turnover, not profit, which catches a lot of side-hustlers off guard : a freelance designer billing £1,200 with £900 of expenses still crosses the threshold and must register, even though their taxable profit is only £300. The second classic scenario is leaving employment to go full-time self-employed, where the registration document typically sits alongside a settlement agreement and a final P45. A third pattern is the gig economy worker reclassified as self-employed after platform changes, which became significantly more common after the Uber BV v Aslam line of authorities reshaped worker status analysis.

Two edge cases deserve attention. First, the dual-income case : someone employed under PAYE who develops a side business. Tax is collected through the existing Self Assessment return, but registration as a sole trader is still required, with Class 2 NICs added to the calculation. Second, the cessation followed by restart case. A person who previously traded, deregistered, and is now starting a new venture must use Form CWF1 rather than starting the registration journey from scratch, because their Unique Taxpayer Reference persists for life. Register as soon as you start trading, not when you remember to. HMRC accepts a small lag, but waiting until the autumn before the deadline compresses everything into one stressful window. If you are also taking on staff, a separate PAYE scheme must be opened, and our UK employment contract templates cover the documentation a small employer needs from day one.

Key clauses included in our template

The document is structured to mirror the order in which HMRC processes the registration and to leave a defensible audit trail. Each clause is short on its own, but together they form a record that survives bank queries, mortgage applications, accountancy handovers and HMRC compliance checks five years out.

- The covering letter to HMRC opens the file. It states your full legal name, address, National Insurance number, the start date of trading, and the nature of the business in plain English. It is dated and signed in wet ink, and a copy is retained. The letter is not strictly required when you register online, but it materially helps if you ever need to evidence the date you treated yourself as having commenced trade, which is the linchpin of badges of trade analysis.

- The CWF1 declaration block applies to anyone already within Self Assessment for another reason, typically rental income or a previous self-employment. The clause is reproduced with prompts for each box, and a brief note on what HMRC does with each field. The completed CWF1 can be sent online or by post to HMRC Self Assessment, BX9 1AS.

- The trading name declaration records the name under which you will invoice and contract. UK law allows a sole trader to trade under a name different from their legal name, but section 1202 of the Companies Act 2006 obliges you to disclose your legal name and an address for service on all business stationery and correspondence. The clause anchors the "Joanna Smith trading as Smith Bookkeeping" convention.

- The record-keeping starter clause lists the categories HMRC expects you to retain for six tax years : sales invoices, purchase receipts, bank statements, mileage logs, asset registers and home-office calculations. It is the closest thing in the document to operational guidance, and it is calibrated to the Making Tax Digital for Income Tax obligations now in force.

- The registration checklist is the cover sheet of the file, used to tick off each step : Government Gateway account created, NI number located, business activity SIC-equivalent description drafted, CWF1 submitted where applicable, UTR received, online tax account activated, first quarterly MTD update calendared. The checklist also flags the £90,000 VAT trigger and links the file across to a Companies House incorporation if the trader later upgrades to a limited company using our Companies House IN01 application form.

Regional considerations

The sole trader regime is set centrally by HMRC and applies across the four nations of the United Kingdom, but the practical environment differs enough that a one-line answer would mislead.

England. Most sole traders register through the Government Gateway and receive their Unique Taxpayer Reference by second-class post within ten working days under HMRC's published service standards. Local authority licences sit on top of HMRC registration and are not part of it : a food trader needs registration with the local environmental health team, a private hire driver needs council licensing, and a property letting business may engage selective licensing schemes that override the simple sole trader baseline. None of these displace HMRC registration ; they sit alongside it.

Scotland. The Scotland Act 2016 devolved the income tax rates and bands payable on non-savings, non-dividend income, so a Scottish-resident sole trader pays the Scottish Rate of Income Tax on trading profits while still paying Class 2 and Class 4 NICs to HMRC at UK rates. The registration mechanics with HMRC are identical, but tax planning differs noticeably above the higher rate threshold. Scottish trading-name disclosure under section 1202 Companies Act 2006 applies in the same terms.

Wales. Welsh-resident sole traders are within the Welsh Rates of Income Tax under the Wales Act 2014, which currently leaves the marginal rates aligned with England but reserves the power for divergence. Bilingual stationery is not legally required for a sole trader, although it is good practice in the public sector supply chain, and Welsh-language correspondence with HMRC is available on request.

Northern Ireland. Sole trader registration with HMRC operates on the same Westminster basis. The notable divergence is VAT on goods moving between Great Britain and Northern Ireland under the Windsor Framework, which can affect a NI-based sole trader trading goods across the Irish Sea. Service-based sole traders, who form the bulk of new registrations, are unaffected. Where a sole trader operates from let commercial premises, the lease itself sits outside HMRC's remit and is governed by the Landlord and Tenant Act 1954 if in England or Wales, with our commercial lease agreement template for England and Wales covering the security-of-tenure regime that applies.

How to fill out this sole trader registration

The journey on Captain.Legal opens with the basic identification data : your full legal name as it appears on your passport or driving licence, your National Insurance number, your residential address, and the address from which the business will operate when these differ. From there, the form asks for the commencement date of trading, which is a question worth taking seriously because it anchors the entire registration. The accepted approach is the date you first invoiced, signed a contract, took payment, or otherwise held yourself out to the world as in business, whichever came first ; speculative preparatory activity does not yet count.

The next step covers the trading name and the business activity, written in language a non-specialist would understand, since this description is what an HMRC officer reads first. The form then branches : if you have ever filed a Self Assessment return, the CWF1 path is selected and the document is preloaded with your existing UTR. If not, the standard registration route generates the covering letter and the checklist tuned to a first-time registrant. VAT, PAYE, and Construction Industry Scheme prompts appear conditionally : you only see them if your answers indicate they apply. The output is a downloadable Word file you can edit further, plus a PDF you can sign and post, mirroring the dual-format approach used across our UK personal legal documents. The whole journey takes about ten minutes once your NI number is to hand.

Common mistakes to avoid

The error we see most often is the late notification. People underestimate how easy it is to drift past the 5 October deadline of the second tax year, and the failure to notify penalty under Schedule 41 FA 2008 bites hardest when there is unpaid tax behind it. The fix is procedural : register the moment you decide you are trading, even if you are still below the £1,000 threshold, because voluntary early registration is free of consequences and locks in the date. The second mistake is misclassifying gross income as profit. The trading allowance is computed on the gross figure ; netting expenses against it and concluding "I'm under £1,000" is a recipe for an unwelcome HMRC letter two years later, when third-party data from payment platforms, marketplaces and banks lands on a compliance officer's desk.

The third mistake is treating the trading name as a brand only. Section 1202 of the Companies Act 2006 requires a sole trader's legal name and a business address for the service of documents to appear on all written business communications, including invoices, websites and order confirmations. Solely displaying "Smith Bookkeeping" without the "Joanna Smith t/a" prefix is a quiet but real breach. The fourth is forgetting the National Insurance picture. Class 2 contributions feed your state pension entitlement, and a low-profit year without a voluntary contribution leaves a gap that can prove expensive at retirement. Check your NI record annually through your personal tax account. The fifth is keeping receipts in a shoebox. From April 2026, Making Tax Digital for Income Tax Self Assessment requires digital record-keeping and quarterly submissions for many sole traders ; the shoebox era has ended in slow motion, and starting the digital habit at registration is far easier than retrofitting it three years in. If your business outgrows sole trader status and you incorporate, our UK articles of association template under the Companies Act 2006 covers the next chapter.

Frequently Asked Questions

40 verified reviews · 50 000+ downloads

- Immediate access to the document

- PDF + Word download

- Compliant with 2026 legislation

- Reviewed by lawyers

You might also like